Welcome to another Logistics News Update.

The Strait of Hormuz remains operational but constrained, with controlled vessel movement and ongoing congestion, South Africa’s main container routes are not directly impacted but the global effect is clear through higher oil prices, increased insurance costs, and pressure on freight pricing. Brent crude remains above $100 per barrel, and with continued uncertainty, there is no short-term relief expected. The April fuel increase is now flowing through the system, with a real risk of further increases into May There are also signals of potential escalation, including discussions around restrictions on vessels linked to Iranian ports, at this stage there is no full blockade and vessel traffic continues, but the situation remains fluid and could change quickly. For South Africa, this means sustained upward pressure on transport, distribution, and input costs, this is a structural shift in the market. Businesses should plan for continued cost pressure, ongoing volatility and greater flexibility in routing and pricing decisions. The risk is no longer just cost; it is also where cargo is going and how secure that route and market is.

Agri & Transport Summary

South Africa’s agricultural export season is gaining momentum, particularly in citrus, with volumes expected to increase further over the coming weeks. While production and demand remain strong, the focus is now shifting beyond cost toward market risk and routing uncertainty. The ongoing instability in the Middle East is starting to directly impact export planning, particularly for shipments into the Gulf region. The Middle East remains a key market for South African citrus, and exporters are becoming more cautious about committing cargo into the region. The risk is not only demand, but also routing, delays and the potential for cargo to be diverted mid-transit. This introduces additional cost, longer transit times, and increased exposure for perishable goods.

From a logistics perspective, the system remains stable and well prepared for the season. Industry coordination and port readiness have improved, with infrastructure and planning in place to support increased export volumes.

Port performance is holding, with Durban operating efficiently and Cape Town remaining weather-sensitive but within normal parameters, the pressure point is no longer at the port, but in decisions made before cargo moves.

The key focus for exporters is now risk management, this includes reviewing market exposure, building flexibility into routing and ensuring contingency plans are in place for key export destinations. As volumes increase, success this season will depend on managing both cost and market uncertainty, not just execution.

Let’s Learn – Why route and market decisions now carry more risk than pricing

Many exporters focus on cost and timing when planning shipments, in the current environment, where you send your cargo and how it moves is becoming just as important as the cost itself.

Why this matters now:

With ongoing instability in the Middle East, key trade routes and markets are becoming less predictable. Cargo moving into certain regions may face delays, rerouting or even diversion to alternative markets. This creates uncertainty not only in delivery timelines but also in final realised pricing and customer commitments.

Where the risk shows up:

• Cargo being diverted to alternative markets at additional cost

• Longer transit times due to routing changes

• Increased exposure to spoilage for perishable goods

• Delays in delivery impacting customer commitments and cash flow

Your Approach:

Do not plan based on cost alone. Review your market exposure, understand routing risks, and build flexibility into your shipment planning. In a volatile environment, the right decision before cargo moves is more valuable than reacting after it is already in transit.

Logistics & Trade Headlines

- Fuel pressure remains the dominant cost driver: Diesel increases are now flowing through the supply chain, with no short-term relief expected as oil remains elevated and geopolitical risk persists.

- Global shipping risk shifting toward routing and market uncertainty: The Strait of Hormuz remains operational but constrained, with vessel delays and controlled passage impacting normal flow.

- No direct disruption to South Africa’s main trade lanes: Asia to South Africa container routes remain stable, with the impact continuing to be indirect through cost, insurance, and network adjustments rather than physical delays.

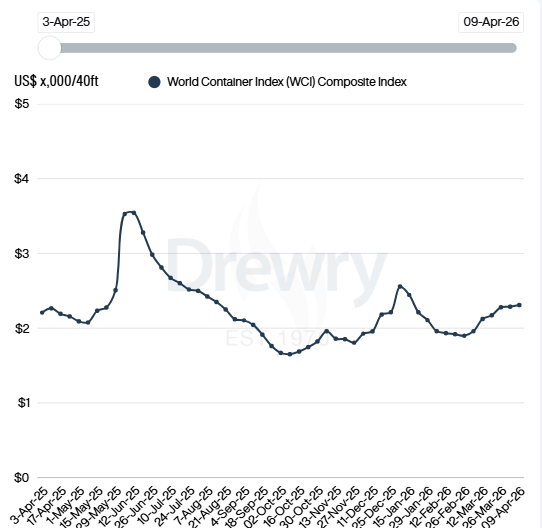

- Freight rates stabilising at elevated levels: The Drewry World Container Index remains around $2,300 per 40ft container, indicating that the market has absorbed recent disruption.

- Bunker costs and surcharges remain elevated: Carriers continue to apply additional charges, with a risk that these become embedded beyond the current disruption period.

Airfreight demand softening while rates remain firm: Global volumes are flat to slightly down, but rates remain elevated due to higher jet fuel costs. - Port performance stable but volumes lower this week: South African container throughput declined week on week, reflecting timing and reporting factors rather than congestion.

- Durban and Cape Town operating within normal parameters: Vessel queues remain stable with no significant backlog, although Cape Town remains weather sensitive.

- Rail performance under pressure: Reduced rail volumes out of Durban continue to shift cargo onto road, increasing exposure to fuel costs.

- Border conditions stable with marginal shifts: South African border crossing times increased slightly, while SADC crossings improved, highlighting ongoing structural inefficiencies across regional corridors.

NEWS

Gulf war could squeeze SA’s citrus exports

Terry Gale, chairman of Exporters Western Cape.

South Africa’s citrus industry is heading into the 2026 export season with strong growth expected, but the war in the Middle East is creating uncertainty at a critical time. Writing in Business Day, Terry Gale highlights that exporters are concerned the timing of the conflict could directly affect the citrus season, which is only now beginning, while earlier fruit exports were largely completed before the escalation. The biggest concern is the Strait of Hormuz, a key global shipping and oil route. While not a primary container route for South Africa, its disruption is driving fuel prices, insurance costs, and broader logistics risk. Terry Gale notes that exporters are “very apprehensive” about committing cargo into an unstable market where routing and delivery conditions can change quickly.

The Middle East remains an important export market for South African citrus, and instability in the region introduces both commercial and operational risk. Exporters are concerned about cargo being diverted mid-transit to alternative markets such as India or Bangladesh at significantly higher cost, with an added risk of delays and spoilage for perishable goods. Beyond market access, the war is also impacting the cost structure of exports. Rising oil prices are feeding directly into fuel, shipping, and inland transport costs. With most citrus moved by road to port, this creates immediate pressure on margins and overall export competitiveness.

The outlook remains cautious, while the industry is still expecting growth, success will depend on how the geopolitical situation develops. The key risk is no longer production, but the ability to manage cost, routing and market uncertainty in a volatile global environment.

Source: Adapted from Sunday Times Business

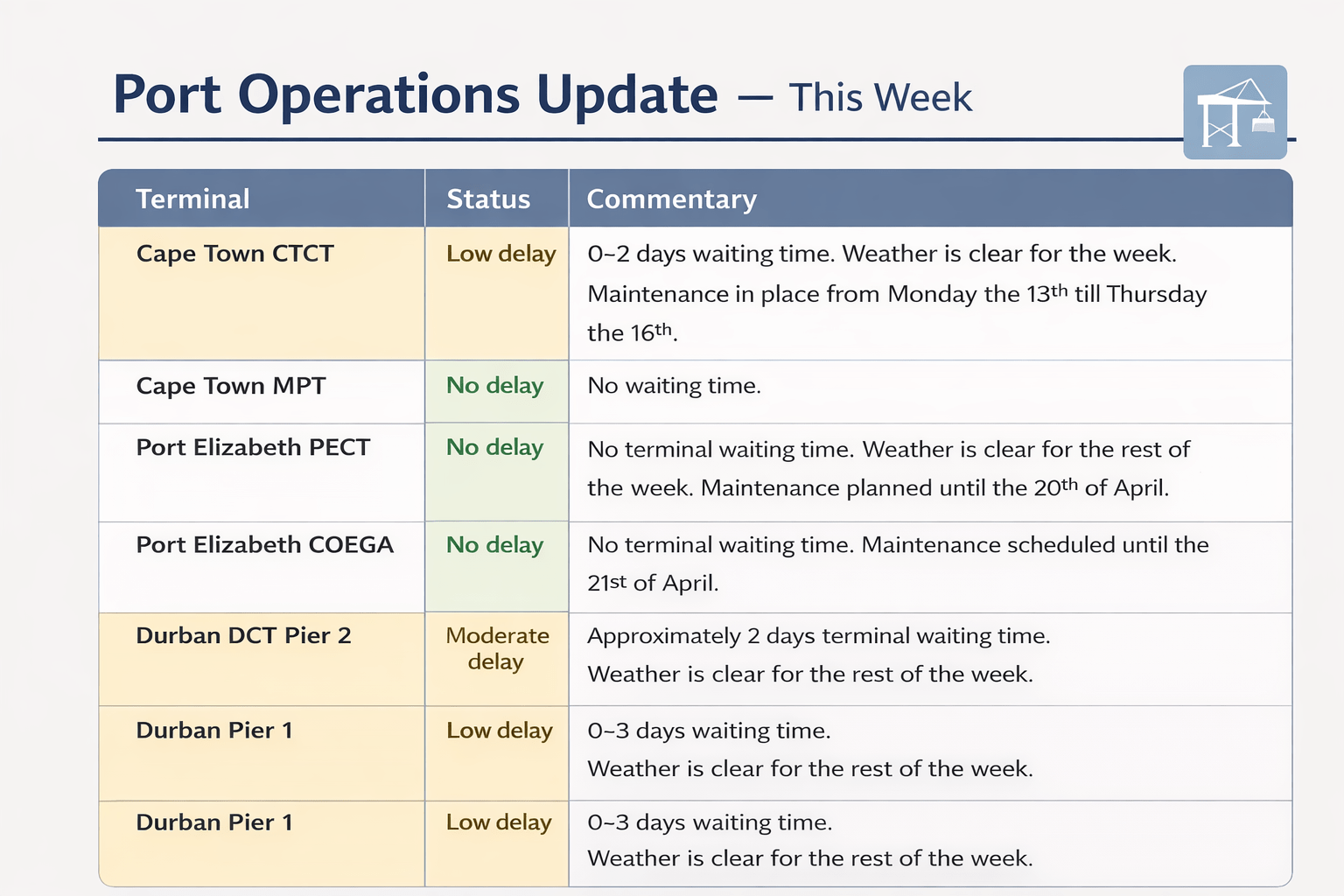

Port Operations Summary: – Port Update:

Key Highlights from Last Week’s Discussions – 5th April 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port performance remained stable, although overall volumes declined following recent increases.

• Total container volumes decreased by approximately 12% week on week to 46,489 TEUs

• An average of 6,641 TEUs handled per day, down from the previous week

• Cape Town experienced minor weather delays but maintained strong berth occupancy and equipment availability

• Durban operations remained stable, with vessel queues unchanged and limited anchorage pressure

• Ngqura saw increased vessel activity, while Port Elizabeth experienced lower volumes and slower performance

Key Insight:

Port operations remain stable with no congestion risk. The decline in volumes reflects timing and reporting factors rather than operational weakness.

Air Cargo

Airfreight volumes softened this week after recent growth.

• Total air cargo volumes decreased by approximately 5% week on week to 7,319 tons

• Inbound volumes remained relatively stable, while outbound volumes declined more significantly

• Volumes remain above last year and pre-pandemic levels despite the weekly decline

• Global air cargo demand remains weak, but rates continue to rise due to elevated jet fuel costs

Key Insight:

Airfreight demand is softening, but pricing remains elevated due to cost pressure rather than demand strength.

Road and Border Crossings

Road and border conditions remain stable, with slight shifts in performance across corridors.

• South African border crossing times averaged approximately 11 hours, slightly up week on week

• SADC border crossings improved to approximately 5.8 hours, down week on week

• Lebombo corridor volumes declined slightly, with truck movements down around 4% week on week

• Queue and processing times remained stable, supported by improved coordination at key borders

Key Insight:

Border performance remains functional, with marginal improvements regionally, although structural inefficiencies persist.

Ocean Freight and Global Shipping

Global shipping remains stable but constrained by geopolitical disruption and cost pressure.

• Container freight rates increased marginally by approximately 1% to $2,309 per 40ft container

• The Strait of Hormuz remains operational but highly constrained, with traffic significantly reduced and over 800 vessels still delayed

• War-risk premiums, bunker costs and routing constraints continue to support freight rates globally

• No system-wide capacity collapse observed, with networks adjusting through controlled routing and risk management

Key Insight:

The global shipping environment remains stable from a capacity perspective, but heavily constrained by risk and cost factors.

Strategic Outlook

The market remains firmly cost-driven. While operational performance across ports and corridors is stable, fuel, energy and geopolitical risk continue to drive pricing across the supply chain. Businesses should focus on managing cost exposure and maintaining flexibility, as volatility is being driven by external factors rather than physical disruption.

Global Freight Rates

Drewry’s World Container Index showed only marginal movement this week, holding at elevated levels at approximately $2,300 per 40ft container. This indicates that the market has stabilised in the short term, with earlier increases now being absorbed rather than accelerating further. The underlying pressure remains firmly cost-driven.

On the Asia – Europe trade, rates remain stable with no significant upward movement this week, carriers continue to manage capacity through selective blank sailings, maintaining pricing discipline as fuel and operational costs remain high, the focus has shifted from pushing rates up to holding current levels in a volatile environment.

On the Transpacific trade, rates are also broadly flat, reflecting a balanced market where demand is steady but not driving pricing. Cost pressures, particularly bunker fuel and operational adjustments, continue to underpin rate levels, preventing any meaningful decline.

The impact of the Middle East conflict is now more clearly reflected in cost structures rather than rate spikes. War-risk premiums, higher bunker costs and routing adjustments are being absorbed into pricing, with carriers focusing on cost recovery rather than aggressive increases. South Africa’s primary Far East trade lanes remain operational and unaffected from a routing perspective.

Overall, the market remains stable from a capacity perspective but continues to operate under sustained cost pressure. Freight rates are expected to remain firm in the short term, with any further movement likely to be gradual and driven by fuel and geopolitical developments rather than demand.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”