Welcome to another Logistics News Update.

The global logistics environment remains stable from an operational perspective, but the underlying risk has not eased. There are still no clear signs of de-escalation in the Middle East and while major trade lanes remain open cost and uncertainty continue to move through the system. Ongoing diplomatic discussions have started but there is no clear indication that these will deliver any short-term outcome.

For South Africa, the impact remains indirect, but it is now embedded in higher fuel costs elevated insurance and ongoing pressure on freight pricing. Locally, port performance remains stable, and the agricultural export season is building as expected but the margin for error is reducing as volumes increase.

Agri & Transport Summary

South Africa’s agricultural export season is gaining momentum particularly in citrus with volumes increasing across the supply chain. Production and demand remain stable supported by new orchards coming into production and improved export readiness across the industry.

The Middle East remains a key area of uncertainty and exporters are showing caution when committing cargo into the region. The risk is not only cost or routing but also timing and reliability particularly for shipments moving into markets where conditions can change quickly.

From a logistics perspective the system remains stable with Durban operating efficiently and Cape Town remaining weather-sensitive but within normal parameters. As volumes increase delays in transport documentation or coordination will have a greater impact on delivery timelines.

Cost remains a key pressure point, with most agricultural exports moving inland by road higher fuel prices continue to impact transport costs and overall margins. As volumes build the focus remains on maintaining consistency in execution and managing exposure to both cost and market risk.

Let’s Learn – (APN) Advance Import Payments and why the reference matters

When importing into South Africa, advance payments to foreign suppliers are regulated under exchange control. These payments must be reported and later matched to the actual import of goods.

What this means:

When you make an advance payment, the transaction is captured through the banking system under Balance of Payments (BoP) reporting. This creates a reference number linked to that payment, which is used to track it through the system.

Why this matters:

The bank is required to ensure that the advance payment is matched to a corresponding import within a prescribed period. This is done using customs documentation submitted after the goods arrive. If the payment and shipment are not correctly linked, it can trigger queries or compliance issues.

Where the risk shows up:

• Payments not matched to the correct import entry

• Delays in clearance or document processing

• Queries from the bank on outstanding advance payments

• Potential compliance issues if imports are not properly acquitted

What to take from this:

Always speak to your forex specialist when you are not 100% sure as they are equipped to assist you with this. Also, ensure that all payment references provided by the bank are retained and shared with your clearing agent. Align your commercial invoice, Bill of Lading, and customs entry to the payment. In importing, control depends on linking the payment, documentation, and cargo correctly.

Logistics & Trade Headlines

- Fuel pressure remains the dominant cost driver: Elevated oil prices continue to filter through the supply chain, with no short-term relief expected and ongoing pressure on transport and logistics costs.

- Geopolitical risk remains unresolved: The Middle East situation shows no clear signs of de-escalation, maintaining pressure on oil, insurance, and global supply chains.

- Strait of Hormuz remains operational but constrained: Vessel movement continues under controlled conditions, with ongoing uncertainty around potential escalation.

- No direct disruption to South Africa’s main trade lanes: Asia to South Africa container routes remain stable, with the impact continuing to be indirect through cost and network adjustments rather than physical delays.

- Freight rates holding at elevated levels: The Drewry World Container Index remains around $2,300 per 40ft container, reflecting a stable but cost-supported market.

- Bunker costs and surcharges remain elevated: Carriers continue to apply additional charges, with a risk that these become embedded into longer-term pricing structures.

- Airfreight demand softening while rates remain firm: Global volumes are flat to slightly down, but rates remain elevated due to sustained jet fuel costs.

- Port performance stable as volumes increases: South African ports continue to operate within normal parameters, with no major congestion reported as export volumes build.

- Durban and Cape Town operating efficiently: Vessel queues remain stable with no significant backlog, although Cape Town remains weather sensitive.

- Rail performance remains under pressure: Reduced rail volumes continue to shift cargo onto road, increasing exposure to fuel costs.

- Border conditions stable with marginal shifts: South African border crossing times remain slightly elevated, while SADC crossings show minor improvement, highlighting ongoing structural inefficiencies.

NEWS

Strait of Hormuz at a tipping point after US seizes vessel

Tensions in the Strait of Hormuz have escalated sharply following the seizure of an Iranian-flagged cargo vessel by US forces, marking a significant shift in the conflict. According to Freight News article, the incident followed a prolonged standoff and has raised concerns that the fragile ceasefire and ongoing diplomatic efforts may collapse. Iran has already indicated possible retaliation, placing further pressure on an already unstable situation.

This development is not just political, it has direct implications for global shipping, vessel movement through the Strait has become increasingly unpredictable, with reports of delays, reduced traffic, and heightened security risks. Recent data shows that shipping activity has slowed significantly, with some vessels turning back or avoiding the region altogether as tensions increase.

The biggest impact remains on energy. The Strait of Hormuz is one of the world’s most critical oil transit routes, and any disruption immediately affects global supply. Following the latest escalation, oil prices have reacted with increased volatility, reinforcing upward pressure on fuel, insurance, and overall logistics costs globally.

For South African importers and exporters, the impact remains indirect but significant. Our primary trade lanes are still operational, but the cost of moving goods continues to rise as carriers adjust for fuel, risk, and uncertainty. The key takeaway is that this is no longer a short-term disruption. It is an evolving risk environment that will continue to influence pricing, planning, and market decisions across the supply chain.

Source: Adapted from FreightNews

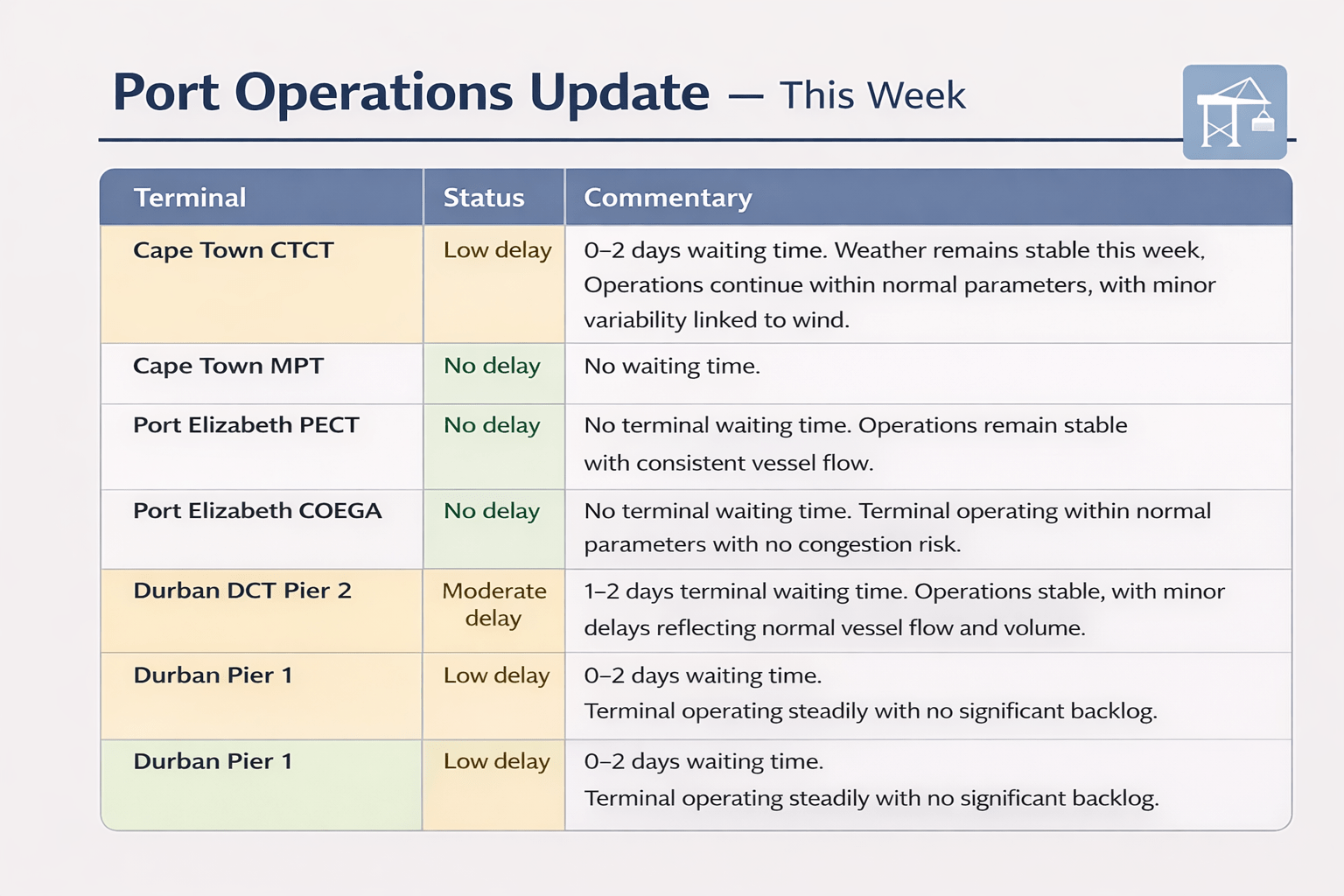

Port Operations Summary: – Port Update:

Key Highlights from Last Week’s Discussions – 12th April 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port performance remains stable, with volumes declining following recent increases.

• Total container volumes decreased by approximately 11% week on week to 47,377 TEUs

• Cape Town improved with no weather delays, while Durban remained stable with no congestion

• Eastern Cape volumes softened, with some maintenance and equipment constraints

Key Insight: Ports remain stable with no congestion risk. Volume changes are timing related, not operational weakness.

Air Cargo

Airfreight volumes declined, particularly on exports.

• Total volumes decreased by approximately 15% week on week to 6,256 tons

• Outbound volumes dropped more sharply, while inbound softened slightly

• Rates increased to around $3.10/kg despite lower demand

Key Insight: Demand is softening, but rates remain elevated due to fuel and capacity constraints.

Road and Border Crossings

Road conditions improved locally, with mixed performance regionally.

• South African border times improved to approximately 10.3 hours

• SADC crossings increased to approximately 6.7 hours

• Cross-border volumes increased month on month

Key Insight: Local performance is improving, but regional inefficiencies continue to create delays.

Ocean Freight and Global Shipping

Global shipping remains constrained by geopolitical risk.

• Gulf-bound capacity down approximately 48%

• Transit times extended by 10–14 days

• Fuel remains elevated in the mid-$90 per barrel range

Key Insight: The system remains stable, but cost and transit time pressure continue to impact global supply chains.

Strategic Outlook

Operations remain stable, but cost and geopolitical pressure persist. Businesses should focus on flexibility, planning and managing fuel and routing risk as conditions are unlikely to ease in the short term.

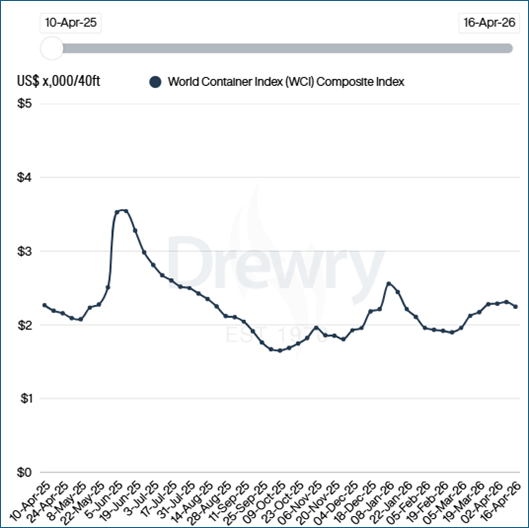

Global Freight Rates

Drewry’s World Container Index softened slightly this week, decreasing to approximately $2,246 per 40ft container. This confirms that while rates remain elevated, the market is not currently accelerating, with pricing being supported by cost rather than demand growth.

On the Asia – Europe trade, rates remain stable with limited movement. Carriers continue to manage capacity through selective blank sailings, maintaining pricing discipline as fuel costs and operational risk remain elevated. The focus remains on protecting margins rather than pushing rates higher.

On the Transpacific trade, rates are also broadly flat. Demand remains steady but not strong enough to drive increases, with pricing supported by underlying cost pressure, particularly bunker fuel and network adjustments linked to geopolitical risk.

The impact of the Middle East situation continues to be reflected in cost structures rather than direct disruption. War-risk premiums, elevated bunker costs and longer routing continue to influence pricing globally. South Africa’s main Far East trade lanes remain operational, with the impact continuing to be indirect through cost rather than physical delays.

Overall, the market remains stable from a capacity perspective but constrained by cost. Freight rates are expected to remain firm in the short term, with any movement likely to be gradual and linked to fuel prices and geopolitical developments rather than a surge in demand.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”