Welcome to another Logistics News Update.

This week’s update shows a logistics environment that is still moving but becoming more expensive and less forgiving. Freight rates have continued to rise; port performance improved in parts and cross-border delays remain a material concern for cargo owners moving through regional corridors.

Brent crude has come down sharply from the highs seen earlier in the year and was trading closer to US$100 per barrel on 25 May. This is positive for fuel-price sentiment, but it is too early to assume a direct or immediate reduction in diesel and petrol costs because local prices still depend on the exchange rate, under-recovery, taxes, levies, and the timing of the fuel price cycle.

Locally, port operations improved overall with total container volumes increasing by approximately 5% week on week to 42 364 TEUs. The recovery was not evenly spread across the network, with Ngqura and Port Elizabeth showing strong volume improvement while Durban remained more mixed, supported by better landside performance but still under pressure on waterside volumes. Cross-border performance weakened this week, with South African border crossing times increasing to around 9.2 hours and SADC regional crossing times increasing to around 7.0 hours. This matters because border delays do not only affect delivery timing. They also affect fleet planning, transport cost, stock availability, and regional supply chain reliability.

The broader message for importers and exporters is that planning discipline matters more than ever. The cheapest freight rate, the quickest route or the easiest booking option can become costly very quickly if the routing is weak, the documentation is late, the handover is poor or the cargo is not properly managed through each stage of the movement.

The common theme across this week’s update is simple: the supply chain is still functioning, but the cost of poor execution is increasing. Clients should be paying close attention to landed cost, rate validity, transport planning, documentation accuracy, border risk, and enough flexibility in their timelines to manage disruption before it becomes additional cost.

NB: PVoC compliance remains a key importer risk: Importers of listed products from China should be engaging suppliers now, because once enforcement increases after the transition period, missing conformity documentation could create delays, storage costs, and customs release problems.

Agri & Transport Summary

South Africa’s agricultural sector is moving into this week with logistics resilience again becoming a central issue. Recent NAMPO 2026 coverage highlighted strong participation from the farming sector while also pointing to difficult operating conditions, rising input costs, and the need for better efficiency across the agricultural value chain. NAMPO 2026 attracted 81 822 visitors and more than 910 exhibitors, showing that confidence and investment interest remain present in the sector but the underlying message for logistics is that producers are still operating in a high-cost environment where transport planning, equipment availability, cold chain control and route-to-market reliability can directly affect margins.

Cold chain discipline remains a major issue for fresh produce exporters, with rising diesel and electricity costs, stricter export requirements and pressure on South Africa’s logistics network putting cold chain management under the spotlight. For exporters, the risk does not start at the port. It starts much earlier in the chain, from on-farm cooling and packing through to inland transport, depot movement, container availability, and final vessel connection.

The road transport environment is also becoming more important for agricultural planning, particularly as rail reform continues to move slower than many cargo owners would like and more freight remains dependent on long-haul road movement. Recent logistics reform commentary noted that more than half of South Africa’s freight logistics reforms were not progressing according to schedule, which means exporters and producers still need to plan around road capacity, diesel exposure, driver availability, and corridor reliability rather than assuming rail recovery will provide short-term relief.

There was some positive transport infrastructure news this week, with CHARGE launching its first off-grid solar-powered electric vehicle charging station on the Johannesburg to Durban N3 corridor. This is not yet a major freight solution, but it is relevant because the N3 remains one of South Africa’s most important commercial transport routes and energy security is becoming part of transport planning.

The practical takeaway for agricultural exporters is that logistics planning needs to start earlier and be managed more tightly this season. Delays in cooling, uplift, inland movement, or port connection can quickly move from an operational inconvenience to a margin problem. Exporters should review transport bookings, cold chain handovers, delivery windows, and contingency plans before cargo is ready to move, not after the pressure has already reached the depot or terminal.

Logistics & Trade Headlines

- Import compliance is becoming a bigger cost risk: South Africa is moving into a tougher trade and import-control environment, with more focus on tariffs, product compliance, and trade defence measures. For importers, the risk is no longer only the freight rate. Incorrect classification, missing documents, or late supplier compliance can now affect landed cost, customs release, and delivery timing.

- PVoC should not be left until September: Importers of listed products from China should start engaging suppliers now, because once enforcement increases after the transition period, missing conformity documentation could create customs stops, storage costs, release delays, and demurrage exposure. The practical issue is simple: if the supplier is not ready before shipment, the importer carries the risk after arrival.

- New steel duties show why landed cost must be checked before ordering: Recent steel duty changes have again shown how quickly import costs can shift while cargo is already in the pipeline. Importers should confirm tariff codes, duty exposure, and possible trade remedies before placing orders, not only when the goods are already on the water.

- Agricultural cargo remains exposed to transport and market-access risk: The grain and fresh produce sectors remain under pressure from logistics delays, tariff uncertainty, and high inland transport dependence. For exporters, this means margin protection is not only about production. It depends on cold chain control, transport availability, port timing, and access to the right export markets.

- Rail reform is moving but road dependence remains the reality: Open-access rail reform remains positive for the long term, but it is not yet a short-term fix for cargo owners. Importers and exporters should still plan around road capacity, diesel exposure, driver availability, and corridor reliability rather than assuming rail recovery will remove current transport pressure.

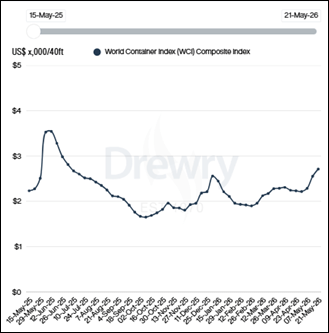

- Freight rates continue moving upward: Drewry’s World Container Index increased by approximately 6% to US$2 712 per 40ft container, with Asia-Europe rates again leading the increase. The key issue is that rates are being supported by carrier capacity management, blank sailings, higher FAK levels and geopolitical risk rather than strong underlying demand.

- Hormuz risk is not resolved: Oil prices have softened on improved market sentiment, but the Strait of Hormuz and wider Middle East situation remain a major risk factor for global shipping, fuel, insurance, and carrier operating costs. Clients should treat the improvement in sentiment as positive but not as a resolved logistics risk.

- Regional corridor performance remains a planning risk: Renewed attention on SA-Botswana border reform highlights the importance of border efficiency for regional trade. Cross-border delays affect truck turnaround times, delivery reliability, stock availability, and final transport cost, especially where cargo moves through already pressured corridors.

- AGOA gives exporters breathing room but not certainty: The AGOA extension gives eligible South African exporters short-term customs certainty into the United States, but it should not be treated as a permanent solution. Exporters should use the extension period to review eligibility, documentation and US market exposure before the next policy decision creates another pricing or market-access risk.

Let’s Learn – Why the cheapest freight rate can become the most expensive option.

Many importers look at the freight rate first because it is the easiest number to compare, but the lowest rate on paper is not always the lowest cost in practice. A cheaper option can quickly become expensive if it comes with weak routing, poor transit times, limited space, bad communication, or no one taking proper control of the shipment once it starts moving.

In practical terms:

The freight rate is only one part of the total logistics cost. The real cost sits in the full movement, including origin handling, freight, destination charges, customs clearance, port costs, transport, storage, demurrage risk, and the time it takes to get the cargo delivered.

Where people get caught:

- Choosing a cheaper sailing with a longer or unreliable transit time

- Not checking whether destination charges are included or excluded

- Accepting a rate without understanding port congestion or routing risk

- Booking late and then paying more to recover time

- Missing documentation deadlines and losing the saving through storage or demurrage

- Comparing quotes that do not include the same services or charges

Quick example:

An importer may save R3 000 on the ocean freight rate but lose far more if the shipment is delayed, misses the planned delivery window or attracts storage and demurrage because the routing, documents or handover were not properly managed.

Takeaway:

The cheapest freight rate is only useful if the shipment still moves correctly, clears correctly, and delivers on time. Importers should compare the full landed cost and the execution risk before choosing a rate, because in logistics the cheapest option can become expensive very quickly when something goes wrong.

NEWS

AGOA Extension Brings Short-Term Customs Certainty

The AGOA extension has given South African exporters short-term customs certainty on duty-free access into the United States, after a US presidential proclamation formally embedded the extension into customs processes. This means eligible South African exports can continue receiving preferential tariff treatment under AGOA until 31 December 2026.

The extension applies retroactively from 1 October 2025, after AGOA had previously expired on 30 September 2025. South Africa remains an AGOA-eligible country under the short-term extension, which means exporters in qualifying sectors have some breathing room while longer-term trade policy discussions continue. The proclamation is important because it gives customs authorities and trade agencies the mechanism needed to apply the revised tariff treatment in practice. It also extends key supporting provisions for African apparel exporters, including the regional apparel programme and the third-country fabric provision.

For South African exporters, the commercial benefit is short-term certainty rather than long-term security. The extension helps protect current access to the US market, but exporters should not assume that future access is guaranteed beyond the extension period. Documentation accuracy, tariff eligibility, and market planning remain important because any future change to AGOA could affect landed cost, pricing, and competitiveness.

Source: Adapted from FreightNews

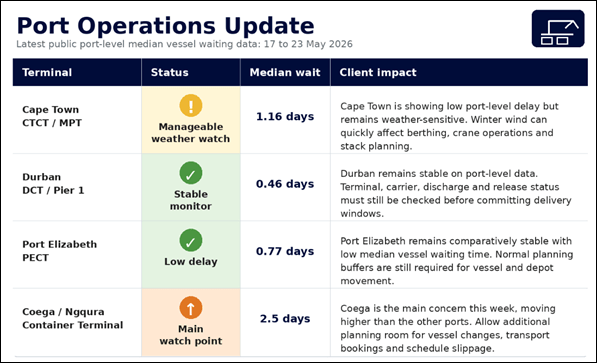

Port Operations Summary: – Port Update:

South African port operations remain manageable this week, but the picture is uneven across the network. Durban is currently the most stable of the main container ports, while Cape Town is operating with relatively low reported delay but remains exposed to wind and winter weather variability. The main watch point is Coega, where public port-congestion data is showing materially higher delay than the other South African ports. GoComet currently shows Coega at 14 days, Durban at 3 days, Cape Town at 1 day and Port Elizabeth at 1 day.

Cape Town should still be treated as weather-sensitive even though the current delay reading is low. Winter conditions can quickly affect vessel berthing, crane operations, and stack planning, especially when wind impacts the terminal window. For clients, the risk is not that Cape Town is currently in crisis. The risk is that planning windows can tighten quickly when weather disruption overlaps with vessel bunching or inland collection delays.

Durban remains relatively stable compared with the rest of the network, with current public congestion data showing a lower delay than Coega but still enough to require vessel-by-vessel monitoring. This is important because Durban performance can look stable at port level while individual terminal, carrier or stack conditions still create timing pressure. Importers should avoid committing delivery dates until vessel arrival, discharge status and carrier release timing have been checked.

Coega is the key concern this week. The latest public congestion reading is significantly higher than the other South African ports and that makes the Eastern Cape the main operational watch point. Even where Port Elizabeth is showing low delay, the Coega reading means clients moving through the Eastern Cape should allow additional planning room for vessel changes, depot movement, transport bookings, and possible schedule slippage.

The practical message for clients is that South African ports are still functioning, but execution needs to be managed closely. The port risk this week is not a broad national shutdown. It is uneven performance, weather exposure, Eastern Cape delay risk and the need to confirm terminal and carrier status before committing to delivery windows.

Key Highlights from Last Week’s Discussions – 17 May 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port operations improved this week, with overall container throughput increasing despite weather disruption in some regions and weaker waterside volumes at Durban’s container terminals.

• Total container volumes increased by approximately 5% week on week to 42 364 TEUs

• An average of 6 052 TEUs was handled per day, up from 5 747 TEUs the previous week

• Cape Town Container Terminal volumes declined by 27% week on week to 10 843 TEUs although the terminal still reported strong waterside performance and stable equipment availability

• Ngqura Container Terminal recovered strongly, increasing by 93% week on week to 11 481 TEUs despite some weather delays earlier in the week

• Port Elizabeth Container Terminal increased by 51% week on week to 4 772 TEUs

• Durban Pier 1 volumes declined by 6% week on week to 13 093 TEUs although truck turnaround time improved and equipment availability strengthened

• Rail cargo out of Durban increased by 31% week on week to 2 791 containers

• DGT advised that revised slot appointment allocations would apply from 20 May 2026, with import slots split between 24-hour and 48-hour releases and export, reefer, IMDG and empty slots reviewed on a four-hourly basis where capacity allows

Key Insight: Port performance improved overall but the recovery was not evenly spread. The Cape and Eastern Cape showed stronger waterside momentum while Durban remained more mixed, with landside performance improving but waterside volumes still under pressure.

Air Cargo

Airfreight volumes softened again this week, although global pricing and annual demand remain elevated and ORTIA received a positive long-term infrastructure signal.

• Total international air cargo volumes decreased by approximately 2% week on week to 5 935 tons

• Inbound air cargo declined from 3 749 tons to 3 713 tons

• Outbound air cargo declined from 2 320 tons to 2 221 tons

• Global air cargo softened for a second week in early May as Asia Pacific volumes normalised after Super Golden Week and the Mother’s Day flower surge faded

• Global average air cargo pricing declined week on week to approximately US$3.22/kg but remained materially higher on a year-on-year basis

• ACSA advanced the environmental authorisation process for ORTIA’s proposed New Cargo Precinct, which is intended to add approximately 750 000 tons per annum of cargo-handling capacity and around 75 000 m² of warehouse space

Key Insight: Airfreight demand is softer in the short term, but the market remains structurally expensive compared with last year. ORTIA’s proposed cargo precinct is positive for long-term capacity but it will not relieve current pricing or service pressure immediately.

Road and Border Crossings

Cross-border performance weakened this week, with longer queue times, longer transit times and continued operational pressure across several SADC corridors.

• South African border crossing times increased to approximately 9.2 hours, up around 13% week on week

• SADC regional crossing times increased to approximately 7.0 hours, up around 35% week on week

• Cross-border queue time averaged approximately 7.4 hours, up from 6.6 hours the previous week

• Average cross-border transit time increased to approximately 7.3 hours, up from 5.5 hours the previous week

• Total indirect border delay costs were estimated at approximately R559 million for the week, slightly down from around R576 million despite longer average delays

• Lebombo truck volumes normalised, increasing by 9% week on week to approximately 1 465 heavy goods vehicles per day

• Persistent delays continued at Groblersbrug while scanner-related congestion at Kanyaka and Kasumbalesa created severe pressure, with queues reportedly reaching up to 16 km

Key Insight: Border delays remain a major commercial risk even when total delay cost improves slightly. The pressure is not only the average waiting time but the unpredictability across corridors, scanners, tolling proposals and inconsistent processing.

Ocean Freight and Global Shipping

Global shipping remains under pressure from geopolitical disruption, carrier capacity management, and uneven demand, with freight rates continuing to rise despite a fragile demand environment.

• Drewry’s World Container Index increased by approximately 6.2% to US$2 712 per 40ft container

• The index has increased by almost US$500 per 40ft container over the last three weeks

• Asia-Europe rates firmed sharply, with Shanghai-Rotterdam up 15% and Shanghai-Genoa up 10%

• Transpacific rates also edged higher, with Shanghai-New York up 2% and Shanghai-Los Angeles up 1%

• Carriers continue using blank sailings, FAK increases and PSS announcements to protect rates ahead of peak season

• Hormuz disruption remains a major global shipping risk, with the report noting that daily vessel transits have fallen sharply from pre-conflict levels

• The Iran conflict is also feeding into energy, insurance, air cargo, and broader logistics cost pressure

Key Insight: Freight rates are rising because of risk, capacity management, and cost pressure rather than strong underlying demand. Importers should not assume current rate increases are only seasonal as geopolitical risk and carrier behaviour remain the bigger drivers.

Strategic Outlook

The local logistics network improved in parts this week, but the operating environment remains fragile. Container volumes recovered, rail out of Durban improved and ORTIA’s cargo infrastructure plans are positive for the long term, but border delays, Durban waterside pressure, fuel exposure, and global freight rate increases continue to create execution risk. Businesses should focus on earlier planning, careful transport coordination, rate validity, documentation accuracy and enough flexibility to manage port, border, and carrier disruption before it turns into additional cost.

Global Freight Rates

Drewry’s World Container Index increased by approximately 6.2% this week to US$2 712 per 40ft container, extending the upward movement seen over the last three weeks and taking the index almost US$500 higher over that period. The latest increase was driven mainly by higher Asia-Europe rates while Transpacific rates also moved up slightly as carriers continued tightening capacity ahead of the peak season.

On the Asia-Europe trade, rates increased sharply as early peak-season demand, higher FAK levels and limited blank sailings supported further upward pricing. Shanghai to Rotterdam increased by approximately 15% to US$2 773 per 40ft container while Shanghai to Genoa increased by approximately 10% to US$4 082 per 40ft container. On the Transpacific trade, rate increases were more modest than last week but still positive. Shanghai to New York increased by approximately 2% to US$4 317 per 40ft container while Shanghai to Los Angeles increased by approximately 1% to US$3 385 per 40ft container. Drewry also noted that seven blank sailings had been announced on the Transpacific trade for the following week, which points to tighter available capacity and gives carriers room to keep pushing higher FAK levels.

The Middle East and Strait of Hormuz situation remains a major risk factor in the background, not because it has directly disrupted South Africa’s main container trade lanes but because it continues to affect risk pricing, bunker exposure, insurance costs, and wider carrier operating costs. The attached BUSA/SAAFF update also notes that the current shipping environment is being shaped by geopolitical disruption, carrier capacity management, and uneven demand rather than strong underlying trade growth.

Overall, the freight market remains operationally stable, but the pricing trend has strengthened again. The important point for importers is that rates are now being driven by a mix of early peak-season movement, blank sailings, higher FAK levels, fuel exposure, and geopolitical risk, which means clients should avoid assuming that current rate increases are temporary or easy to reverse.

Final Thoughts

The logistics environment is still functioning but the margin for error is getting smaller, freight rates are rising, border delays remain inconsistent, port performance is uneven and compliance requirements are becoming more important.

For importers and exporters, the practical response is not to wait until cargo is already moving before dealing with risk. Rate validity, tariff classification, supplier documents, transport planning, delivery windows, and border exposure should be checked before the shipment is committed.

The businesses that manage these details early will protect cost, avoid unnecessary delays, and reduce the risk of storage, demurrage, and delivery failure. If you are placing new orders, reviewing freight rates, or moving cargo through regional corridors, speak to us before committing to routing, pricing, or delivery timelines.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”