Welcome to another Logistics News Update.

If you’ve never read a Logistics News Update before, don’t miss this one!

Just when you thought trade and logistics in South Africa couldn’t get any more complicated — boom! A headline grabs attention: “Freight industry prepared to fight state-owned cabotage.” (see the full story below under NEWS) – so, what does this mean? Simply put, if you’re shipping goods to South Africa, you could soon be forced to use a government-owned shipping line for domestic transport. Under the proposed Merchant Shipping Bill B12-2023, cargo arriving from international waters must first be offloaded at a designated port (for example, Durban) before being transported by a state-controlled vessel to its final destination, such as Port Elizabeth or Cape Town. This isn’t just speculation—it’s a bill before Parliament, first tabled in 2022, and it’s packed with changes that could seriously disrupt the industry.

This should concern every importer, exporter, and logistics provider. Here’s why:

- Higher costs – Additional handling and state-run transport could push up prices.

- Longer delays – More red tape and dependency on one shipping line could mean extended transit times.

- Limited competition – With foreign vessels restricted from moving goods between SA ports, efficiency could take a major hit.

This bill isn’t just about regulations—it’s about who controls freight movement in South Africa. If it goes through, your supply chain could face massive disruptions.

– See our only news story this week.

Let’s Learn: Understanding Cabotage and Merchant Haulage

Cabotage in South Africa means that the shipping line takes full responsibility for delivering your cargo from the port to its final destination. In contrast, merchant haulage allows you to choose your own haulier at your preferred price to handle the inland transport. It’s important to note that when opting for merchant haulage, you must pay a fee to the shipping line to release the container before transporting it yourself. In this week’s story, cabotage follows the same principle—but instead of road transport, it applies to sea transport between local ports.t of April

NEWS

Freight industry prepared to fight state-owned cabotage

13th March 2025 – Eugene Goddard

South Africa’s private-sector freight industry is fully prepared to oppose the Merchant Shipping Bill in its current form, Terry Gale of Exporters Western Cape (EWC) told a trade gathering in Cape Town on Wednesday night. Speaking at a presentation by the Hong Kong Trade Development Council, the chairman of the EWC said: “We understand that the Bill is heading back to parliament, and I want to tell you that we are going to fight it.”

Asked whether he was referring to the section in the Bill proposing cabotage, the practice of disallowing commercial container lines from calling at more than one port on a country’s coast, Gale said yes. He explained what the Bill was proposing. “They want to establish hub ports. In other words, a shipping line coming from Europe, for example, will have one port call in South Africa.” He said that a box ship berthing in Durban with containers destined for Cape Town would have to offload those containers for trans-shipment to the final port of destination.

As the Bill stands, it is understood that the intention is for the state to launch an SA-flagged fleet that will handle the coastal redistribution of containers. According to more than one private-sector source Freight News has approached, the idea is to launch a state-owned entity (SOE) that will be responsible for trans-shipment along the country’s coast.

“It’s a ludicrous idea,” an ocean freight stakeholder said. “It’s primarily used in countries like the US where the entire logistics chain is far more advanced than South Africa’s. Currently, it’s simply not feasible at all. If our government didn’t have the reputation, it has when it comes to running SOEs, state-owned transhipment along our coast might have been worth considering. It’s obviously meant to generate more revenue for our fiscus. But you only have to look at what happened to Eskom and Transnet to realise that the Bill, as it pertains to cabotage, is a bad idea.”

Gale said: “Think of what happened to Safmarine,” the SA-owned shipping line that was eventually taken over by Maersk in 1999 and entirely absorbed into the Danish line’s brand. “The government had an opportunity with one of the most incredible shipping lines in the world, but they lost that opportunity.”

He said a government-enforced transhipment system in South Africa would add significant cost to the entire supply chain by adding complexity at hub ports, as it would require multimodal logistics for the redistribution of containers. He pointed out that one only had to look at what was currently happening at the country’s ports to realise that cabotage on SA’s coast wouldn’t work….

– Source: FreightNews

WEEKLY SNAPSHOT

- Port of Cape Town Implements Digital Tracking System: The Port of Cape Town introduced a new digital container tracking system to improve operational efficiency. This system provides real-time updates to stakeholders, aiming to reduce delays and streamline cargo handling processes.

- Air Freight Demand Surges: Airports Company South Africa (ACSA) reported a 15% increase in air freight volumes compared to the same period last year. The surge is attributed to a rise in e-commerce and the pharmaceutical sector’s growth, highlighting the importance of air cargo in meeting time-sensitive delivery requirements.

- Trucking Industry Faces Fuel Price Hike: The South African trucking industry is grappling with a 5% increase in diesel prices, effective from 16th March. This escalation is expected to impact transportation costs, prompting logistics companies to reassess pricing strategies and explore fuel-efficient alternatives.

- Durban Port Congestion Eases: Efforts to alleviate congestion at the Port of Durban have yielded positive results, with waiting times for vessels reduced by 30%. Collaborative initiatives between port authorities and private stakeholders have been instrumental in enhancing cargo flow and reducing bottlenecks.

- New Customs Regulations Implemented: The South African Revenue Service (SARS) implemented new customs regulations aimed at simplifying clearance procedures and enhancing compliance. These changes are expected to reduce administrative burdens and facilitate smoother trade operations.

- Logistics Sector Embraces Green Initiatives: Several leading logistics companies announced initiatives to reduce carbon emissions, including the adoption of electric delivery vehicles and investment in renewable energy sources. These efforts align with global sustainability trends and reflect a commitment to environmentally friendly practices.

On The Ground Report

Cape Town port was delayed by four days last week, they have also started to do split berths in Cape Town. Durban has only two split berths but is operating normally.

The South Africa – Europe Container Service (SAECS) has faced multiple disruptions in recent weeks, leading to schedule delays. These have been caused by: Extreme weather conditions in South Africa, Terminal inefficiencies, Rotterdam strike/go-slow action, Heavy congestion, and bad weather in European hubs. To mitigate delays, the Santa Rita/250N will omit Cape Town, sailing directly to Europe from Durban. Cape Town imports will be transhipped via Mehuin, which will take Santa Rita’s position in Cape Town, ensuring continuous export coverage. Despite these challenges, SAECS has successfully maintained service continuity throughout the Deciduous Fruit Export Season, and measures are in place to stabilise schedules for the upcoming Citrus Export Season. Source: Maersk

Port Operations Summary: – Port Update:

SOUTH AFRICAN PORTS

DURBAN

The port has experienced windy weather during the week.

- Pier 1 : 0-3 days delay

- Pier 2 : 0 -2 days delay

- Durban Point : 3 days delay

CAPE TOWN

The port has experienced strong winds during the week. The port is still experiencing intermittent Southeasterly winds.

- CTCT : 4-9 days with intermittent wind experienced.

- MPT : 3 days with intermittent wind experienced.

PORT ELIZABETH

The port has experienced windy weather during the week.

- PECT : 0 days delay Source: SACO

Global Freight Rates

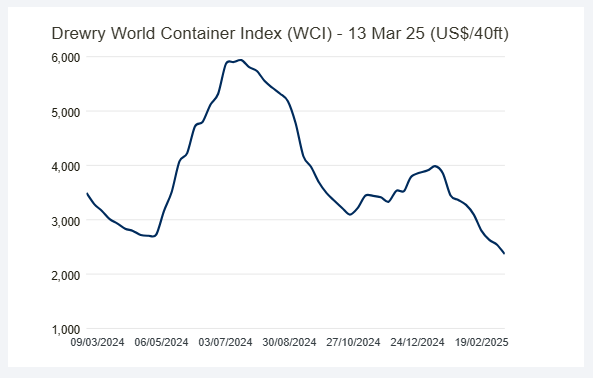

- As of March 13, 2025, Drewry’s World Container Index (WCI) experienced a 7% decline, bringing the composite index to $2,368 per 40-foot container. This marks a 77% decrease from the pandemic peak of $10,377 in September 2021 and is the lowest level since January 2024. Despite this decline, the index remains 67% higher than the pre-pandemic average of $1,420 in 2019. The year-to-date (YTD) average composite index stands at $3,205 per 40-foot container, which is $321 higher than the 10-year average of $2,884, a figure inflated by the exceptional rates observed during the 2020-2022 COVID period. As of March 13, 2025, Drewry’s World Container Index (WCI) experienced a 7% decline, bringing the composite index to $2,368 per 40-foot container. This marks a 77% decrease from the pandemic peak of $10,377 in September 2021 and is the lowest level since January 2024. Despite this decline, the index remains 67% higher than the pre-pandemic average of $1,420 in 2019. Drewry anticipates that freight rates will continue to recede in the coming weeks as shipping capacity increases.: Source: Drewrey

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”