Welcome to another Logistics News Update.

We are pleased to see that diesel is coming down, only by a little, but every cent counts. We hope to see some positive results in the next week out of the Middle East. However, this week’s update is more positive on volumes but still cautious on execution. Ports moved more cargo, airfreight improved and some border delay costs eased but the system is not yet smooth enough to assume everything will move without pressure.

Locally, the latest BUSA/SAAFF update shows total container volumes up by approximately 46% week on week to 61 829 TEUs, with an average of 8 833 TEUs handled per day. That is a strong improvement but Durban landside congestion, Cape weather exposure, Eastern Cape movement and limited DGT reporting still need to be watched closely.

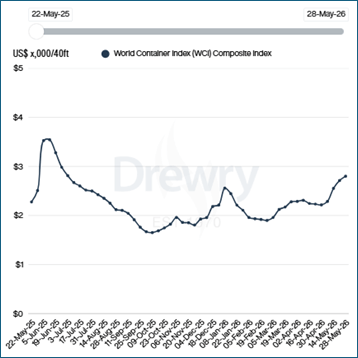

Freight rates also moved up again, with Drewry’s World Container Index increasing by approximately 3% to US$2 800 per 40ft container. Importers should continue checking rate validity, booking windows and routing options before committing landed cost or delivery promises.

Cross-border performance remains mixed. Overall delay costs improved but South African border crossing times increased to around 10.4 hours, while the broader SADC region improved to around 5.9 hours. This shows why regional cargo still needs proper planning, especially where documentation gaps, system outages or long queues can affect delivery.

The common theme this week is simple: movement has improved but control still matters. Importers and exporters should check rates, documents, tariff exposure, shipping instructions, border risk, and delivery windows before cargo is committed, not after the pressure has already reached the port, depot, or border.

Agri & Transport Summary

South Africa’s agricultural exports started 2026 on a strong footing, with first-quarter exports increasing by approximately 11% year on year to US$3.7 billion. The improvement was supported by higher export volumes and better prices across several key products, including grapes, apples and pears, maize, wine, stone fruit, sugar, wool, fruit juices, nuts, and avocados. This is positive for the sector, but it also reinforces the importance of reliable logistics because stronger export volumes place more pressure on ports, inland transport, cold chain execution, and route-to-market planning.

The stronger export performance does not remove the pressure on producers. Recent agricultural commentary warned that South African agriculture is being reshaped by climate shocks, logistics constraints, tighter regulation and changing global trade dynamics. For exporters, this means competitiveness is no longer only about producing a good crop. It depends on whether cargo can be cooled, packed, moved, cleared, and delivered into the right market without delays that reduce margin or product quality.

The grain sector is also under pressure, with wheat farmers facing uncertainty linked to delayed tariff decisions, rising input costs, weak profitability and shrinking plantings. This matters from a logistics point of view because tariff uncertainty affects planning, pricing, and procurement decisions, while weaker profitability makes transport cost, storage cost and delivery timing even more important for producers and traders.

From a policy and market-access perspective, the focus remains on export resilience, competitiveness and protecting existing markets while looking for new opportunities. For agriculture, this links directly to logistics execution because export growth only creates value if the supply chain can support it. Road transport, port efficiency, cold chain capacity, documentation accuracy, and market access all need to work together if exporters are going to protect margins in a more uncertain trading environment.

The practical takeaway for agricultural exporters is that the opportunity is still there but the margin for error is small. Strong export numbers are encouraging but producers and exporters should not treat volume growth as a guarantee of profitability. Transport bookings, cold chain handovers, tariff exposure, delivery windows, and documentation should be checked early because weak execution can quickly turn a good export opportunity into a cost problem.

Logistics & Trade Headlines

- PVoC risk has become more practical for importers: A new PVoC HS code list has raised concern that cargo could be detained unnecessarily if the codes are applied too broadly. Importers of affected products from China should not wait until September because missing or unclear conformity documentation could create customs stops, storage costs, release delays, and demurrage exposure.

- China export agreement creates opportunity, but procedures still need clarity: South African exporters are still waiting for clearer procedures on how the new China-Africa Economic Partnership Agreement will work in practice. The agreement may create duty-free access for qualifying exports into China, but exporters still need certainty around certificates of origin, rules of origin and the exact process before they can rely on the benefit commercially.

- Road freight is under pressure from crime and regulation: The road freight sector is facing a tougher operating environment, with organised crime, cargo theft, regulatory pressure, and Aarto implementation adding risk for transport operators. For cargo owners, this means road freight planning should include route risk, tracking, driver control, and tighter handover processes.

- KZN truck disruption risk highlights corridor vulnerability: A threatened truck slow-down on key KZN routes last week again showed how quickly road freight can be exposed to labour, regulatory and protest-related disruption. The N3 and N2 remain critical corridors and clients moving time-sensitive cargo should allow for contingency planning when corridor risk increases.

- Diesel decreases should provide some transport cost relief: Diesel prices are set to decrease from Wednesday while petrol prices are increasing. This should offer some relief to diesel-dependent transport operators, but the benefit may not flow through immediately or equally across all contracts because transport costs are also affected by route risk, waiting time, fleet availability, and general operating costs.

- Container throughput improved but border delays remain costly: South African container terminals recorded a strong improvement in throughput last week, with average daily volumes rising sharply. The concern is that border delays still carried a material cost for regional cargo movement, which means port recovery does not automatically solve delivery reliability for cargo moving into or out of neighbouring countries.

- UAE cargo now needs earlier documentation planning: Cargo moving into or through the UAE will need to meet a 72-hour shipping instruction deadline from 15 June under the “No Manifest, No Load” policy. Exporters and forwarders moving cargo through UAE-linked routes need to submit shipping instructions on time because non-compliance could result in cargo not being loaded, changed destination, returned cargo or additional penalties.

- Air cargo demand is growing but capacity remains tight: IATA reported that global air cargo demand increased year on year in April while capacity declined. This means airfreight remains useful for urgent cargo, but pricing and space pressure can remain high where geopolitical disruption, fuel costs and limited capacity affect key corridors.

- Freight rates continue moving upward: Drewry’s World Container Index increased again to US$2 800 per 40ft container on 28 May, marking the fourth consecutive week of increases. Asia-Europe and Transpacific rates both moved higher and carriers are still using higher FAK levels, peak-season surcharges, and blank sailings to support pricing.

- Black Sea shipping risk has increased: Maritime risk in the Black Sea has risen after several merchant vessels were targeted in a short period. This is not a direct South African port issue, but it adds to global shipping uncertainty, insurance risk, and wider supply chain volatility.

Let’s Learn, why shipping instructions must be done properly and on time

Many importers and exporters see shipping instructions as a simple admin step, but they are far more important than that. Shipping instructions tell the shipping line what information must appear on the bill of lading and cargo manifest, including the shipper, consignee, notify party, cargo description, container numbers, seal numbers, weights, destination, and any special handling details.

In practical terms:

If shipping instructions are submitted late or with incorrect information, the carrier may not process the bill of lading in time, or the cargo details may not match the documents needed for customs, release and delivery. This can delay the shipment, create extra amendment costs or in more serious cases stop the cargo from being loaded.

Where people get caught:

- Sending shipping instructions after the carrier cut-off

- Using vague or incorrect cargo descriptions

- Giving the wrong consignee or notify party details

- Incorrect container, seal, or weight information

- Not checking whether the bill of lading matches the commercial documents

- Assuming the forwarder or shipping line will correct the details without delay

- Forgetting that some countries and carriers now have stricter manifest deadlines

Quick example:

A shipment may be packed and ready at origin but if the shipping instructions are late or wrong, the carrier may not be able to finalise the manifest before the deadline. The cargo could then miss the planned vessel or require amendments that delay document release and delivery at destination.

Takeaway:

Shipping instructions are not just paperwork. They are part of the control process that allows the cargo to move correctly, be manifested correctly and clear correctly. Importers and exporters should treat shipping instructions as a critical deadline because small mistakes on the documents can quickly become delays, extra costs, and avoidable frustration.

NEWS

Diesel price drop to offer some relief

Diesel dependent transport operators should see some relief this week, with diesel prices set to decrease from Wednesday. According to Freight News, diesel with 0.05% sulphur will decrease by R3.24 per litre while diesel with 0.005% sulphur will decrease by R2.61 per litre. This is positive for road freight operators, especially where long-haul transport, cross-border movements and container deliveries are heavily exposed to fuel cost.

The benefit will not be the same across the whole supply chain. Some transport contracts adjust fuel surcharges quickly while others only adjust after a set review period. In practice, cargo owners should not assume that lower diesel will immediately reduce every transport quote or delivery cost. Route risk, waiting time, fleet availability, tolls, congestion, and border delays still form part of the total transport cost.

Petrol prices are moving in the opposite direction, with both 93 and 95 petrol increasing by R1.43 per litre. Freight News also reported that LP gas and illuminating paraffin will decrease, while the rand strengthened slightly against the US dollar during the review period, helping reduce the basic fuel price contribution. The Department said middle distillates such as diesel and paraffin decreased more than petrol because of lower seasonal demand as the northern hemisphere moves into summer.

For importers and exporters, the practical message is that the diesel decrease is welcome, but it does not remove transport risk. Freight planning still needs to account for port delays, border delays, route disruption, truck availability, and timing. Lower diesel may ease some cost pressure but poor planning, waiting time and missed delivery windows can still wipe out the benefit quickly. Source: Adapted from FreightNews

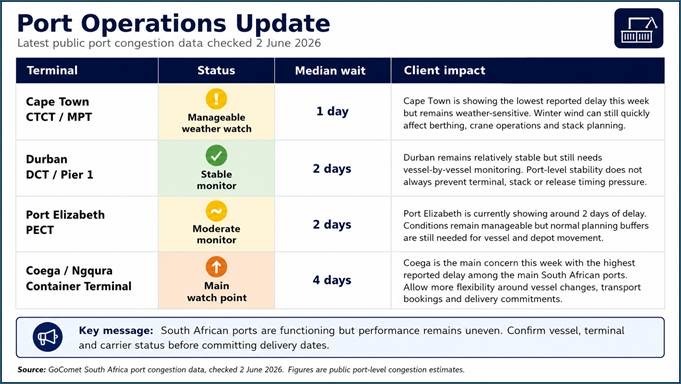

Port Operations Summary: – Port Update:

South African port operations remain manageable this week, but the network is still uneven. Current public congestion data shows Coega as the main watch point at approximately 4 days, while Durban is showing around 2 days, Port Elizabeth around 2 days and Cape Town around 1 day. This suggests that the system is moving but clients should still avoid treating port performance as uniform across the country.

Cape Town is currently showing the lowest reported delay among the main ports, but it should still be treated as weather sensitive. Winter wind and weather can quickly affect berthing windows, crane productivity, and stack planning, especially where vessel bunching or delayed inland collections start building pressure. The current reading is manageable, but Cape Town can change quickly when weather interrupts operations.

Durban remains relatively stable but still needs vessel by vessel monitoring, a 2-day congestion reading is not severe, but it is enough to affect delivery planning where clients are working to tight delivery windows. Durban can look stable at a port level while individual terminal conditions, stack movement, carrier release timing, or transport availability still create delays.

Coega is the main operational watch point this week, with current public congestion data showing a higher delay than the other South African ports. This does not mean all Eastern Cape cargo will be delayed but it does mean clients using Coega should allow more flexibility around vessel changes, depot movement, transport bookings, and delivery commitments. Port Elizabeth is also showing some delay but remains materially lower than Coega.

The practical message for clients is that South African ports are functioning, but execution still needs close control. The biggest risk this week is not a broad port failure. It is uneven performance across ports, weather exposure in Cape Town, higher delay risk at Coega and the need to confirm vessel, terminal, stack, and carrier release status before committing delivery dates.

Key Highlights from Last Week’s Discussions – 17 May 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port operations improved strongly this week, with overall container throughput increasing well above the previous week and most container terminals reporting stronger waterside volumes despite weather-related disruptions and landside pressure.

• Total container volumes increased by approximately 46% week on week to 61 829 TEUs

• An average of 8 833 TEUs was handled per day, up from 6 052 TEUs the previous week

• Cape Town Container Terminal volumes increased by 39% week on week to 15 024 TEUs despite a slower start on the land and rail side

• Ngqura Container Terminal increased by 70% week on week to 19 462 TEUs despite some mid-week weather delays

• Port Elizabeth Container Terminal increased by 58% week on week to 7 525 TEUs

• Durban Pier 1 increased by 15% week on week to 15 001 TEUs with improved equipment availability as new RTGs started supporting the fleet

• Durban Gateway Terminal reporting remains limited following the transition from DCT to DGT although the report estimates waterside throughput declined by around 18% to about 23 000 containers

• Rail cargo out of Durban increased by 25% week on week to 2 955 containers

• Bayhead Road congestion continued through the week, particularly during peak periods, with Metro Police and Transnet teams remaining on site to support traffic flow

Key Insight: Port throughput improved materially this week, but the improvement does not mean execution risk has disappeared. Durban landside congestion, limited DGT reporting, Cape weather exposure and Eastern Cape weather delays still require close vessel, terminal, and transport planning.

Air Cargo

Airfreight improved this week, with international cargo flows through ORTIA increasing and outbound volumes showing the strongest movement.

• Total international air cargo increased by approximately 5% week on week to 6 215 tons

• Inbound cargo increased by 1% week on week to approximately 3 731 tons

• Outbound cargo increased by 12% week on week to approximately 2 484 tons

• Current ORTIA volumes are broadly in line with May 2025 but remain around 6% below the pre-pandemic May 2019 level

• Domestic air cargo performed better in April, increasing by 5% month on month and 24% year on year across the three main terminals

• Global air cargo spot rates remained stable at approximately US$3.67/kg but are still around 48% higher year on year while capacity remains constrained, especially around MESA and Gulf markets

Key Insight: Airfreight is firmer this week but still expensive. Export-driven improvement is positive, but clients should continue to plan early where cargo is urgent, high-value or time-sensitive because capacity and pricing pressure remain in the market.

Road and Border Crossings

The border picture improved in some areas but remains uneven, with total delay costs down while South African-controlled border times worsened.

• Average cross-border queue time decreased by around 1 hour to approximately 6.4 hours

• Average cross-border transit time decreased by around 0.9 hours to approximately 6.4 hours

• South African border crossing times increased to approximately 10.4 hours, up around 13% week on week

• SADC regional crossing times improved to approximately 5.9 hours, down around 16% week on week

• Total indirect border delay costs decreased to approximately R489 million, down around 13% from the previous week

• Lebombo truck volumes increased by 5% week on week to approximately 1 542 HGVs per day

• Queue times at Lebombo improved to approximately 3.7 hours while processing times improved to around 3.4 hours

• Kazungula congestion worsened early in the week, Kasumbalesa delays intensified and the northbound queue reportedly reached around 40 km

• BURS CMS tolling system downtime created additional processing risk because no manual fallback solution was reportedly available

Key Insight: Border costs improved overall but corridor risk remains high. The biggest concern is not only the average delay number. It is the unpredictability caused by system outages, scanning delays, uncleared vehicles, documentation gaps, and long queues on key regional routes.

Ocean Freight and Global Shipping

Global shipping remains shaped by disruption, uneven reliability, and weak carrier profitability, with the Strait of Hormuz still carrying material risk for shipping, fuel, and wider logistics costs.

• Strait of Hormuz traffic remains severely reduced, with the 7-day moving average at around 6.3 vessels compared with 109.9 vessels a year earlier

• The report describes the Hormuz issue as shifting from outright closure risk to delay, detention, rerouting, and commercial uncertainty

• Average operating margins among leading container lines were broadly flat at 5.2% in Q1 2026

• Hapag-Lloyd and Maersk reported negative margins, showing that carrier profitability remains uneven despite disruption-driven rate support

• Global schedule reliability remains uneven, with some lanes becoming more stable while others continue carrying disruption and reallocation pressure

• Container scrapping remains very low, with only 4 456 TEU scrapped in the first five months of 2026, meaning excess vessel capacity still exists in the market

• Global air cargo markets stabilised in week 20, with worldwide chargeable weight up 3% week on week and 2% year on year

Key Insight: Global shipping is not in collapse, but it remains exposed to disruption-led cost pressure. Hormuz, uneven reliability, capacity management, and weak carrier profitability all point to a market where rates and schedules can still move quickly.

Strategic Outlook

This week’s update is stronger on volume performance but still cautious on execution risk. Ports handled materially more cargo, rail out of Durban improved and air cargo volumes increased but Durban landside congestion, uneven border performance, Coega and Eastern Cape weather delays, Hormuz risk and rail system performance remain important pressure points.

Businesses should not treat higher volumes as proof that the system is fully stable. The correct response is to keep planning early, check documentation, confirm vessel and carrier status, allow for border and corridor risk and avoid committing delivery dates before the full movement has been properly checked.

Global Freight Rates

Drewry’s World Container Index increased again this week, rising by approximately 3% to US$2 800 per 40ft container. This is the fourth consecutive weekly increase, and the latest move was driven by higher freight rates on both the Asia-Europe and Transpacific trades. The index has now moved from US$2 286 on 7 May to US$2 800 on 28 May, showing that pricing pressure has built steadily through May.

On the Asia-Europe trade, rates continued moving upward, supported by early peak-season demand and higher market pricing. Shanghai to Rotterdam increased by approximately 3% to US$2 861 per 40ft container while Shanghai to Genoa increased by approximately 4% to US$4 253 per 40ft container. Drewry also noted that only four blank sailings had been announced on the Asia-Europe trade for the following week, which points to relatively stable capacity on that lane.

On the Transpacific trade, rates also strengthened this week. Shanghai to Los Angeles increased by approximately 3% to US$3 473 per 40ft container while Shanghai to New York increased by approximately 6% to US$4 597 per 40ft container. This shows that the pricing pressure is no longer only an Asia-Europe issue and that carriers are still holding stronger rate levels through capacity discipline, FAK adjustments and peak-season positioning.

The Middle East and Strait of Hormuz risk remains an important background factor, not because South Africa’s main container routes have been directly stopped but because the disruption continues to influence fuel exposure, insurance costs, vessel deployment, and carrier operating risk. The latest BUSA/SAAFF update also shows that Hormuz vessel movement remains materially lower than normal, with the 7-day moving average at around 6.3 vessels compared with 109.9 a year earlier.

Overall, the freight market remains operationally functional, but pricing pressure has strengthened again. Importers should avoid assuming that rates will fall back quickly because the current market is being shaped by early peak-season movement, carrier pricing discipline, geopolitical risk, and uneven schedule reliability. The practical response is to check rate validity, booking windows and routing options early before committing landed cost or delivery promises to clients.

Final Thoughts

This week’s message is clear. The logistics environment is still functioning, but the pressure is building in the areas that directly affect cost and execution. Freight rates have moved higher again, port performance has improved but remains uneven, border delays are still unpredictable, and compliance requirements are becoming harder to ignore.

For importers and exporters, the risk is not only whether cargo can move. The real risk is whether it moves with the right rate, the right documents, the right routing, and enough time in the plan to absorb delays. A cheaper freight rate, late shipping instructions, poor tariff classification, weak supplier documentation or missed cut-off can quickly turn into storage, demurrage, amendment costs or missed delivery commitments.

The stronger port volumes reported this week are positive, but they should not be mistaken for a fully stable supply chain. Durban landside pressure, Coega delays, cross-border system issues, Hormuz-related risk, and higher global freight pricing all show that cargo owners still need to manage each shipment carefully from order placement through to final delivery.

The businesses that protect cost in this environment will be the ones that plan early, check rate validity, confirm documentation, understand tariff and compliance exposure, and leave enough room in the timeline for operational disruption. If you are placing new orders, reviewing freight rates, or moving cargo through regional corridors, speak to us before committing to routing, pricing, or delivery timelines.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade™ 360 — your partner in logistics and Exporters Western Cape