Welcome to another Logistics News Update.

As much as we try, we can’t escape the pressure the USA exerts on global logistics. From 14 October, vessels owned or operated by Chinese entities will face steep port-entry fees in US ports. These will start at $50 per net ton and increase to $140 by 2028. US Customs will enforce the policy, and non-compliant vessels may be denied cargo operations or even departure clearance.

We may not understand every motive behind these moves, but we must understand that global trade affects us. The knock-on effects hit freight rates, transit times and container availability. This is a reminder that our planning must stay global, not just local. We’ll continue to monitor developments and advise clients where exposure or opportunity may arise.

What is the news?

- Taiwan has suspended its export curbs on semiconductors to South Africa after diplomatic pushback. The move helps avoid disruption in tech supply chains.

- From 14 October, the US will impose port entry fees on vessels owned or operated by Chinese entities. Charges start at $50 per net tonne and will rise to $140 by 2028. Non-compliant vessels may be blocked from cargo ops or departure clearance.

- A truck fire at the Kazungula border post has raised serious concerns about how dangerous goods are handled. The incident shows the need for stricter control and better processes when moving hazardous cargo across the region.

- A Russian cargo plane, blacklisted under US sanctions, landed in Upington last week. It drew attention due to its restricted status and the unknown nature of its cargo.

- The permit system used by the KZN Department of Transport collapsed, leaving abnormal load trucks stranded for days. Operators waited up to a week just to get movement approvals.

- South Africa is pushing hard for the renewal of the African Growth and Opportunity Act (AGOA), which expired on 30 September. The Government remains confident but stakeholders are watching closely.

Let’s Learn: What Is a “Blank Sailing”?

When booking containers, clients often ask why a vessel suddenly skips a sailing or route. The term for this is blank sailing, and it can directly affect your lead times.

What Is a Blank Sailing?

A blank sailing happens when a shipping line cancels a scheduled port call or an entire voyage. That means your container booking gets delayed, even if it was confirmed.

Why Do Carriers Do This?

- Low demand – If there isn’t enough cargo, carriers remove a sailing to avoid running half-empty vessels.

- Holidays or shutdowns – Around Golden Week in China, for example, factories close and volumes drop.

- Schedule realignment – Carriers may skip ports to make up for delays or rebalance capacity.

How Does It Affect You?

- Your container could miss its planned vessel

- You may face longer transit times

- It can affect delivery commitments and stock levels

How to Avoid Issues:

- Book early during peak seasons

- Use freight forwarders with strong carrier relationships (like TSI)

- Build some buffer into your lead times

- Stay flexible on routes or transhipment options

Key Point: Blank sailings are becoming more common as carriers adjust to weak demand. Planning protects your supply chain from disruption.

NEWS

AGOA expiry will cut exports to US by 21%

Source: FreightNews – Lyse Comins

Africa Feels the Blow as AGOA Expires – Textiles, Citrus, and Vehicle Exports Among the Worst Hit

The African Growth and Opportunity Act (AGOA), which gave duty-free access to the US market for 32 African countries, expired on 30 September after 25 years. The fallout is already visible. African exporters are now facing new tariffs, cancelled orders, and mounting job losses, especially in labour-heavy sectors like textiles and apparel.

What You Need to Know:

- Lesotho: Nearly 60% of its apparel exports went to the US, duty-free under AGOA. Now they face a 15% tariff. The country’s textile sector employs over 40,000 people and is already seeing job losses and order cancellations.

- South Africa:

- Citrus exports now carry a 30% duty, the highest in Africa. That puts 140,000 farm jobs at risk.

- Vehicle exports to the US fell nearly 40% year-on-year in Q2. The ITC warns that our overall US exports could fall 17% by 2029.

- Sector Impact: Apparel and textiles are the hardest hit. Without AGOA, total exports from beneficiary countries to the US could drop 21% by 2029. Other vulnerable sectors include leather goods, processed foods, beverages, and footwear.

Pamela Coke-Hamilton of the International Trade Centre puts it plainly: “This is about real people, real jobs. AGOA was trade, not aid—and the loss is mutual.”

What Now?

While this marks a difficult transition, it’s also a wake-up call. African countries, including South Africa, must:

- Add more value locally before exporting

- Expand intra-African trade

- Build resilience through the African Continental Free Trade Area

WEEKLY NEWS SNAPSHOT

- If AGOA is not renewed, African exports to the US could drop by 21% by 2029. The data comes from the International Trade Centre and highlights what’s at stake for South African exporters.

- SA and US trade negotiators are making progress. A draft deal could be in place by the end of October. This would secure continued access to key export markets under AGOA.

- Global air cargo demand grew by 4.1% in August. Volumes are improving, but rates remain under pressure due to excess capacity and slow economic recovery in key regions.

- A private sector group from South Africa has submitted a trade proposal in Washington. It promotes a “Secure Saldanha Corridor” to link mining and agriculture to global export markets.

- A new digital weighbridge is now operational at Walvis Bay. It will improve truck processing times and support better traffic flow through the port. Source: various

Key Highlights from Last Week’s Discussions – 28th September 2025

Source: BUSA, SAAFF, and global logistics data

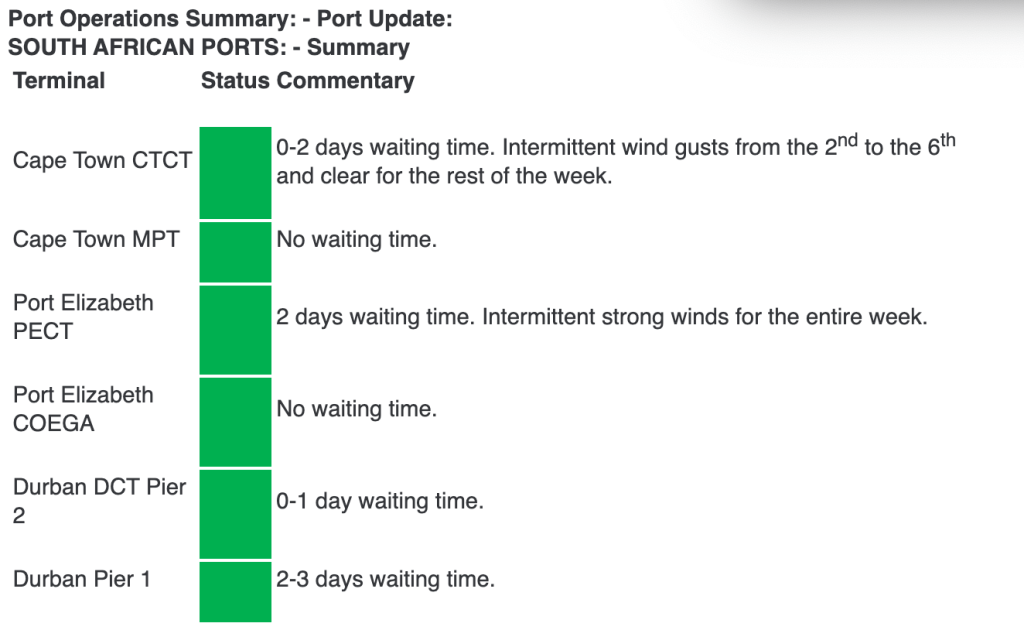

1. Port Operations – Stronger Throughput but Weather Still a Drag

- Total container throughput reached 93,810 TEUs (↑15% w/w), averaging 13,401 TEUs/day, ahead of projections

- Durban Pier 2 eased slightly (↓5% to 33,626 TEUs), while Pier 1 improved (↑21% to 14,521 TEUs).

- Cape Town dropped sharply (↓31% to 11,027 TEUs) due to high swells and equipment issues.

- Ngqura surged (↑151% to 22,208 TEUs) and Port Elizabeth also rose strongly (↑82% to 6,078 TEUs).

- Rail out of Durban improved again, handling 3,884 containers (↑9% w/w).

- Vessel queues at Durban worsened: Pier 2 had seven container vessels waiting, with additional delays for dry bulk, liquid bulk, and breakbulk vessels

2. Air Cargo – Outbound Gains Offset Inbound Dip

- OR Tambo handled ~3,885t inbound (↓8% w/w) and ~3,369t outbound (↑7% w/w), totalling 7,254t (↓2% w/w)

- Despite the dip, levels remain well above 2024 (↑10% y/y) and pre-2019 (↑11%).

- ATNS reported non-standard departures at FAOR due to SID issues, causing delays in sequencing.

- Authorities reinforced compliance with Foreign Operator Permits (FOPs), warning of suspensions for non-compliance

3. Road and Cross-Border – Mixed Border Trends

- Truck flows at Lebombo rose to ~1 489/day (↑4%), but queue times stretched to 5,5 hrs (↑17%) and processing times to 5,3 hrs (↑20%)

- Median crossing times at SA borders improved (↓18% to ~9,4 hrs), but SADC region worsened (↑16% to ~7,3 hrs).

- Severe congestion persisted at Groblersbrug (3–4 day queues), compounded by power outages at Kopfontein and enforcement disputes at Kazungula.

- Zambia lifted its sulphuric acid export ban, while the DRC replaced its cobalt ban with strict quota limits

4. Global Shipping – Rates in Freefall, Trade Tensions Escalate

- Drewry’s Port Throughput Index slipped ↓1,1% in July but remains ↑4,1% y/y, with global growth forecasts upgraded to ↑3,3%

- Regional split: North America surged (+8,3% m/m), Asia contracted (-3,4% to -3,0%), and Africa dipped (-1,9%).

- Freight rates collapsed again: Drewry’s WCI fell ↓7,9% (↓$152) to $1 761/FEU, now ↓52% y/y

- Overcapacity and weak demand fuel recession fears, with mid-October general rate increases unlikely to hold.

- US tariffs on furniture, cabinets, and timber sparked Chinese retaliation threats, heightening trade friction

5. Global Air Cargo – Africa Stays Positive, SAF in Focus

- Global tonnages held steady in mid-September, with Africa–Europe flows up 9% y/y

- Rates edged up to $2,44/kg (↑1% w/w), supported by stronger Africa demand (↑3%).

- Asia Pacific–US volumes slumped ↓20% y/y due to US tariffs and e-commerce restrictions.

- IATA emphasised sustainable aviation fuel (SAF) as critical to the 2050 net-zero goal, but scaling requires faster technology, feedstock security, and policy support

Port Operations Summary: – Port Update:

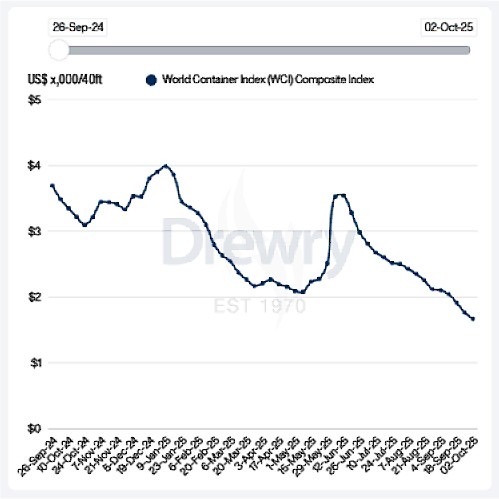

Global Freight Rates

Weekly Container Rate Update – 25th September 2025

Rates Drop Further as Golden Week Disruptions Begin

Drewry’s World Container Index fell another 5% this week to $1,669 per 40ft container, its lowest point since January and the 16th straight weekly decline.

Route-by-Route Snapshot:

- Shanghai – Los Angeles: ↓5% to $2,196

- Shanghai – New York: ↓2% to $3,200

- Shanghai – Rotterdam: ↓7% to $1,613

- Shanghai – Genoa: ↓9% to $1,804

Carriers are responding by blanking sailings and cutting capacity, especially ahead of China’s Golden Week factory closures (1–8 October). Despite these efforts, soft demand is still driving rates down across all major East–West trade routes.

Drewry expects this downward pressure to continue as the supply-demand balance weakens over the coming quarters. Source: Drewrey

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”