Welcome to another Logistics News Update.

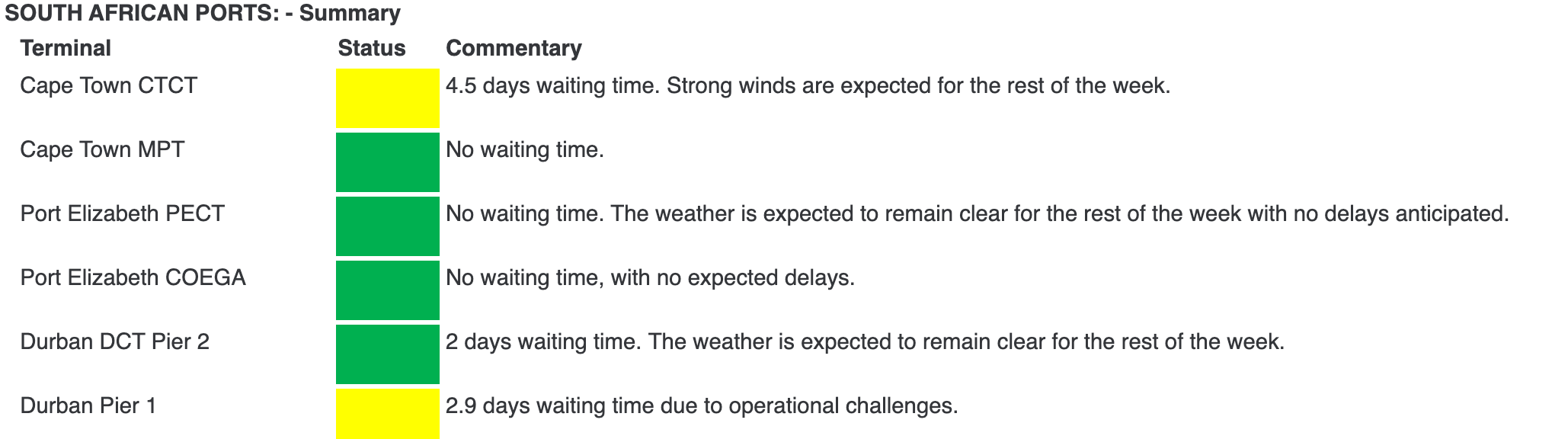

The city we all love (Cape Town) has taken a real pounding from the wind again. We mentioned it last week. This week, we had a few pleasant breaks.

The delays are clear in the port reports and at one point, things were completely out of hand. Our main story this week examines whether the Port of Cape Town requires additional assistance as the wind continues to disrupt operations. Johannesburg has also been pounded with rain and hail, which means the route from Durban to Johannesburg is also affected, so expect delays from both Cape Town and Durban.

There is some good news in the region. Southern Africa has recorded a strong finish to the 2025 lemon season. Growers packed a total of 41.5 million cartons, far above the original forecast. It is an impressive result and positive for the broader citrus sector, which has been under pressure for the past few years.

We also cannot ignore the ongoing tariff landscape. South Africa now faces exclusion from the renewed AGOA agreement. United States Senator John Kennedy has introduced AGOA 2.0 to extend the programme for two years, although South Africa has been singled out because of its current political alignments. Losing AGOA would remove duty-free access for many products and put about 2.8 billion dollars in annual exports at risk. The Bill was introduced on 30 September, just after the original AGOA programme lapsed. This affects duty-free access for 32 countries in sub–Saharan Africa and adds new pressure on exporters who rely heavily on South African ports and logistics corridors.

Trade

- Citrus momentum continues with a strong lemon finish: Southern Africa closed the 2025 lemon season with 41.5 million cartons packed. This is well above the original forecast. The sector notes stable demand across Europe and the Middle East and improved packhouse flow. Exporters have welcomed the stronger finish, although they remain concerned about shipping delays in Cape Town and Durban during the windy period.

- AGOA uncertainty grows after South Africa’s proposed exclusion: The introduction of AGOA 2.0 in the United States has created new pressure for South African exporters. The Bill proposes a two-year extension of AGOA but removes South Africa because of its political position in recent international conflicts. If passed, South Africa would lose duty-free access on about 2.8 billion dollars’ worth of goods, with citrus, wine, automotive parts, and metals carrying the highest risk. Exporters are preparing for a possible tariff shock in early 2026 while hoping for further negotiations.

- Soya and maize exporters report steady regional demand: Regional buyers in Zimbabwe, Botswana and Mozambique continue to draw volumes of maize and soya from South Africa. Prices have stabilised and the border flow has remained steady over the last week with no major congestion reported. Exporters do note longer processing times at Beitbridge because of increased traffic on certain days.

- EU markets show firmer interest in table grapes ahead of peak season: Growers in the Northern Cape and Western Cape are preparing for the first grape exports of the season. Early indications from EU buyers show firmer interest and better pricing than last year. Exporters are watching weather patterns closely and keeping a close eye on shipping schedules, given recent wind delays in Cape Town.

- Logistics constraints remain the biggest swing factor: Across most agri exports, the biggest variable remains logistics. Wind-related stoppages in Cape Town and tight equipment availability in Durban are still creating rollover risk. Exporters are planning earlier load dates and spreading bookings across multiple services to protect market windows. Most expect conditions to stabilise once the current weather system passes.

What is the news

- Wind disruptions remain the main operational pressure at Cape Town: The strong south easter continued to interrupt operations at the Cape Town Container Terminal during the past week, although there were a few windows of better productivity. Several vessels recorded long anchorage waits and delays of more than 24 hours on certain days. This remains the biggest operational challenge for exporters moving through the Western Cape.

- Durban shows more stable performance with steady crane availability: Durban delivered more consistent results across Pier 1 and Pier 2 with improved crane deployment and fewer equipment breakdowns. Truck flow through the terminals was more predictable and vessel working times were stable. Exporters report fewer last-minute schedule changes, which has helped improve planning.

- Transnet continues with targeted upgrades across the ports: The new rubber-tyred gantry cranes at Cape Town are now in active use and additional units are expected over the next few months. Durban continues with maintenance and fleet rehabilitation to lift reliability. These efforts are part of a broader programme aimed at reducing stoppages and lifting throughput ahead of the next peak cycle.

- Global freight markets remain mixed: Spot rates out of Asia softened on some routes, although Europe bound trades held up. Carriers are still adjusting capacity quickly, which makes planning difficult. Most analysts expect rate swings to continue through December as demand slows and blank sailings increase.

- Agricultural exporters prepare for the next export wave: The lemon season ended strongly, and table grape growers are preparing for the first cuts. Exporters in the Northern Cape and Western Cape are watching the weather and shipping schedules closely. The mix of wind delays, tight equipment and strong overseas demand means planning needs to stay tight to protect market windows. Source: FreightNews & IOL

Let’s Learn: What AGOA Means for Exporters and Why Its Renewal Matters

AGOA is one of the most important trade programmes for many African exporters. It gives duty-free access to the United States market for thousands of products. When your goods enter the US at zero duty they land cheaper, which makes them more competitive than products from countries that do not have the same access.

Why AGOA Matters

Many South African industries rely on this duty-free access. Sectors like citrus, automotive parts, wine, steel, and clothing gain a real competitive edge because the tariff saving lowers the landed cost. Buyers in the US choose suppliers who can give them the best margin. AGOA helps South African exporters hold those positions in a very competitive market.

What Happens When a Country Is Excluded

If South Africa is removed from AGOA the duty-free advantage falls away. This means exporters will face normal US import duties. For citrus, this could be more than 15 percent. For automotive components and metals it can be higher. The result is simple. South African products will be more expensive than those from countries that still enjoy AGOA access. Buyers usually shift quickly to lower duty origins to protect their margins.

Why the Current Debate Matters

AGOA 2.0 has been introduced in the US Senate and South Africa has been singled out for exclusion. If this goes through the risk to exporters is immediate. The estimated exposure is around 2.8 billion dollars a year. This includes fruit, wine, metals and several manufactured goods. Exporters need to understand the impact so they can plan early.

What Exporters Can Do Now

• Stay close to your industry body for updated guidance

• Talk to your buyers to understand their duty exposure and plans

• Review your logistics planning so you avoid delays that add cost

• Consider front-loading early-season shipments if the duty change becomes likely

Key Point

AGOA shapes competitiveness in the US market. If South Africa is excluded, exporters will need strong planning and tight logistics to stay competitive while new trade terms are negotiated.

Tariff decisions can shift competitiveness overnight. Understanding how they work helps you plan better, price correctly and stay ahead of your competitors.

NEWS

Does the PoCT need some help against the ‘Cape Doctor’?

28 Nov 2025 – By Eugene Goddard

The Port of Cape Town is once again under pressure as the strong south-easterly winds known as the Cape Doctor continue to disrupt container operations. Vessel dwelling times at the Cape Town Container Terminal remain among the highest in the world. The wind has created long delays at berth and at anchorage and this is slowing the movement of cargo for both exporters and importers.

Transnet has begun adding new equipment to strengthen the terminal. In September, the port received nine new rubber-tyred gantry cranes that can operate in higher wind speeds. They are fitted with anti-sway systems and advanced video technology to improve accuracy and safety. These units are the first of twenty-eight planned cranes that form part of a wider improvement programme.

The upgrades are helping in parts of the operation, but the overall impact has been limited. The past few weeks delivered some of the worst wind stoppages of the season. One week had only a single full day of uninterrupted operations. The week before had two. Several vessels faced waiting times of more than thirty hours and long queues formed at anchor while ships waited for a berth.

Industry observers are questioning how port performance is being measured. Cape Town faces unique weather conditions because of its location at the southern tip of the continent. The cold Benguela current and the warm Agulhas current create a pattern that makes wind disruption inevitable at certain times of the year. Many stakeholders argue that any fair assessment of the port must take these conditions into account instead of comparing Cape Town with ports that operate in calmer environments. Terry Gale from Exporters Western Cape says the industry must compare apples with apples and recognise the climate challenges that come with Cape Town’s position. “It is only natural that the wind would play havoc with the Peninsula.

Source: Adapted from FreightNews

Key Highlights from Last Week’s Discussions – 16th November 2025

Source: BUSA, SAAFF, and global logistics data

1. Port Operations

South African ports handled 69,058 TEUs, down 5% from the previous week. The daily average dropped to 9,865 TEUs from 10,437 TEUs last week.

Breakdown

- Durban Pier 2: 36 670 TEUs (↑16%)

- Durban Pier 1: 12 240 TEUs (↓13%)

- Cape Town: 1 449 TEUs (↓81%) – more than 80 operational hours lost to wind

- Ngqura: 13 139 TEUs (↓10%)

- Port Elizabeth: 0 TEUs

- Durban rail uplift: 2 994 containers (↓14%)

Main Issues

- Cape Town severely constrained by wind, with 80+ hours lost

- Durban impacted by equipment failures and limited crane/straddle availability

- Eastern Cape ports saw vacant berths due to adverse weather and equipment challenges

- Richards Bay constrained by marine equipment failures

Summary

A tougher week across all coastal terminals. Cape Town saw the sharpest decline due to wind. Durban was operational but slower, with rising TTT and staging times. Overall national throughput softened again.

2. Air Cargo

Airfreight volumes picked up again.

Weekly Totals

- Inbound: 4 970 026 kg (↑1%)

- Outbound: 2 891 977 kg (↑4%)

- Total: 7 862 003 kg (↑2%)

Current volumes remain 14% above 2024 and 13% above 2019.

BUSA Cargo Movement Update (202…

Operational Concerns at ORTIA

Some pressure on fuelling operations

Ongoing infrastructure failures

Rising frequency of power, water and baggage system outages

3. Road and Border Crossings

Conditions tightened slightly across regional borders.

Lebombo

- Traffic: 1 372 trucks/day (↓6%)

- Queue time: ~6.3 hours

- Processing time: ~6.2 hours

South African borders overall

- Median crossing time: ~12.0 hours (↓5%)

SADC region (excl. SA-controlled)

- Median time: ~5.7 hours (unchanged)

Hotspots

- Zimbabwe: Heavy rain, washed-out detours, police harassment reports

- Zambia: ASYCUDA failures causing queues

- Beitbridge: Intermittent congestion from road closures and enforcement issues

Estimated Indirect Cost of Delays

- ~$35 million (≈R602 million) for the week (↑19%)

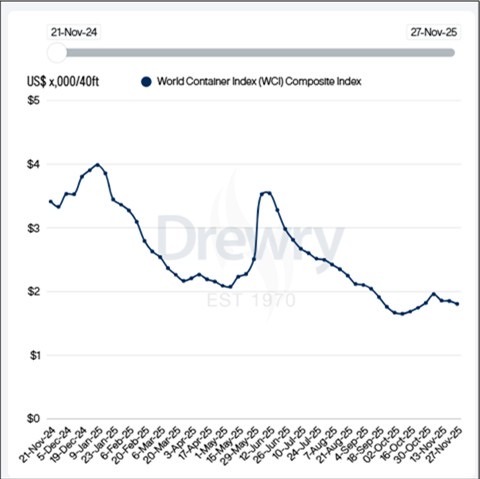

4. Ocean Freight and Global Shipping

- World Container Index: down 0.4% to $1 852/FEU

- Trans-Pacific rates softened

- Asia–Europe rates strengthened

- Global throughput: down 5.6% m/m, up 5% y/y

- MSC fleet: remains at ~7m TEU (≈21% global capacity)

- Schedule reliability: down to 65.2%, delays now averaging 4.98 days

- Scrapping remains low: only 14 vessels demolished YTD

Summary

Rates are stable overall, but they diverge by lane. Global market sentiment has weakened with TEU-mile demand falling below supply. Over-capacity risk continues to build due to the record orderbook.

Port Operations Summary: – Port Update:

Global Freight Rates

Weekly Container Rate Update – 27 November 2025

Drewry’s World Container Index decreased by 2 percent this week to 1 806 dollars for a 40-foot container. The drop is driven mainly by softer rates on the Transpacific and Asia to Europe routes.

On the Transpacific head haul, spot rates continue to fall for the third straight week. Shanghai to New York dropped 6 percent to 2 735 dollars and Shanghai to Los Angeles fell 4 percent to 2 089 dollars. Drewry expects blank sailings on the Transpacific to ease next week, which will increase available capacity. This could lead to a further softening of rates in the short term.

After six weeks of gains, the Asia to Europe trade also saw a decline. Rates from Shanghai to Genoa and Rotterdam fell by 1 percent to 2 300 dollars and 2 165 dollars. Carriers are pushing to lift spot levels by introducing higher FAK tariffs of between 3 100 and 4 000 dollars from 1 December. This is aimed at strengthening pricing ahead of the annual contract negotiation period.

A national strike in Belgium has added pressure to port operations and congestion at the Port of Antwerp. The situation is expected to worsen as some carriers are planning to return to the Suez Canal route. This will increase traffic and affect efficiency, with longer delays and higher spot rates likely.

Drewry’s outlook suggests the global supply and demand balance will weaken over the next few quarters. If normal transits through the Suez Canal resume it could place further pressure on rates as more capacity comes back into the market. Source: Drewrey

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”