Welcome to another Logistics News Update.

If you are importing from China, this is important.

Last month, the Department of Trade, Industry and Competition gazetted a new directive introducing a Pre-Export Verification of Conformity (PVoC) programme under the Standards Act. The programme applies to certain designated products imported from China and requires goods to be tested and certified before shipment to South Africa. Suppliers will need a Certificate of Conformity confirming the goods meet local standards before export.

A transition period is currently in place until 20 September 2026, after which enforcement is expected to increase. Importers bringing in affected products without the required certification may face delays, detentions, and additional compliance costs during the import process. This sits alongside existing NRCS requirements and signals a broader shift toward origin-based compliance.

The important point is that compliance is now moving upstream to the supplier before cargo even ships. Importers should start engaging suppliers early to understand whether their products are affected and whether the required certification process is already in place.

Agri & Transport Summary

South Africa’s agricultural export season is now moving into its higher volume phase, particularly in citrus and deciduous fruit. Export demand remains stable, but the pressure is increasingly shifting toward inland execution as transport costs, equipment positioning and delivery timing become more critical. The Middle East remains a sensitive export market with ongoing geopolitical uncertainty continuing to affect planning decisions. Exporters are monitoring routing reliability closely, particularly for perishable cargo where extended transit times or delays can materially impact product quality and shelf life.

From a logistics perspective the system remains operationally stable. Durban continues to perform consistently while Cape Town remains weather sensitive as winter conditions begin to develop. The biggest operational risk is not congestion, but coordination across transport, documentation and cold chain movement as export volumes increase. Rail constraints continue to place additional pressure on road transport and overall logistics costs. With fuel remaining elevated and most agricultural cargo still dependent on road movement, inland transport remains one of the largest cost risks facing exporters during the current season.

Logistics & Trade Headlines

- South Africa preparing tighter import controls: Government is moving ahead with stronger enforcement against substandard and non-compliant imports, including expanded pre-export verification requirements on selected goods.

- Fuel costs remain elevated: Oil prices continue to trade at volatile levels, maintaining pressure on diesel pricing and inland transport costs.

- Strait of Hormuz remains a key global risk point: Vessel traffic continues through the region, although security concerns and geopolitical tension remain elevated.

- Freight rates holding steady: Drewry’s World Container Index remains relatively stable, with pricing continuing to be supported by fuel and operating costs rather than strong demand growth.

- Airfreight remains under cost pressure: Global demand remains soft, but elevated jet fuel prices continue supporting higher air cargo rates.

- Citrus exports continue to build: Export volumes are increasing as the season ramps up, with ports and cold chain infrastructure currently operating within normal parameters.

- Rail reform pressure increasing: Industry calls for improved rail performance continue as exporters remain heavily reliant on road transport for inland movement.

- Port performance remains stable: Durban and Cape Town continue operating within normal ranges, with no major congestion reported.

- Cape Town entering weather-risk period: Seasonal weather variability is starting to increase operational risk heading into winter.

- Border conditions remain inconsistent: Regional border crossings continue showing mixed performance with ongoing structural and processing delays.

- Inland transport remains the key pressure point: Rising fuel costs and road dependency continue to impact landed cost and export margins across the supply chain.

Let’s Learn – why storage and demurrage costs escalate so quickly

Incoterms are the trade terms on your invoice that decide who arranges transport, who pays which charges and when the risk transfers from seller to buyer, they look like a small detail, but they often explain surprise costs, delays, and claim disputes.

Many importers focus on freight and clearance costs but underestimate how quickly storage and demurrage charges can accumulate once cargo is delayed.

In practical terms:

Demurrage is charged when containers remain at the port or terminal longer than the allowed free time. Storage charges apply when cargo occupies space at the terminal beyond permitted periods. These costs increase daily and can escalate rapidly during delays.

Where people get caught:

- Missing document cut-offs or customs releases

- Delays in payment or cargo collection

- Incorrect or incomplete shipping documentation

- Assuming free days are longer than they are

Quick example:

A shipment delayed by only a few days due to missing documentation can quickly accumulate demurrage storage and transport standing costs, turning a profitable shipment into a loss-making one.

Takeaway:

In logistics small delays become expensive very quickly. Early document control customs readiness and transport planning are often the difference between a smooth clearance and unnecessary cost exposure.

NEWS

Freight rates on steep conflict curve

Double stacked container trains are typically the type of freight trains that will share the standard-gauge corridors with regional rapid transit. Source: Draft National Rail Master Plan

South Africa’s citrus industry is increasing pressure on government to accelerate rail reform, warning that rising logistics costs and continued dependence on road transport are placing significant strain on exporters. Industry representatives have raised concerns that without urgent improvement in rail performance, transport costs will continue to erode competitiveness and place additional pressure on farming margins.

The concern is centred around the country’s freight rail network, where poor reliability and limited capacity continue to force exporters onto road transport. The Citrus Growers Association highlighted that a large portion of freight that should move by rail is currently moving by road due to operational inefficiencies and lack of service reliability.

This is becoming increasingly important as citrus export volumes continue to grow. Higher diesel prices and inland transport costs are already placing pressure on exporters, particularly with the majority of agricultural cargo still moved inland by truck. Industry leaders warned that logistics costs are becoming one of the biggest risks to long-term competitiveness.

Government’s proposed rail reform plans and increased private sector participation are viewed positively by industry, but concerns remain around execution speed and implementation. Exporters are calling for faster progress on rail access, infrastructure investment, and corridor reliability to support future agricultural growth and reduce pressure on the road network.

Source: Adapted from FreightNews

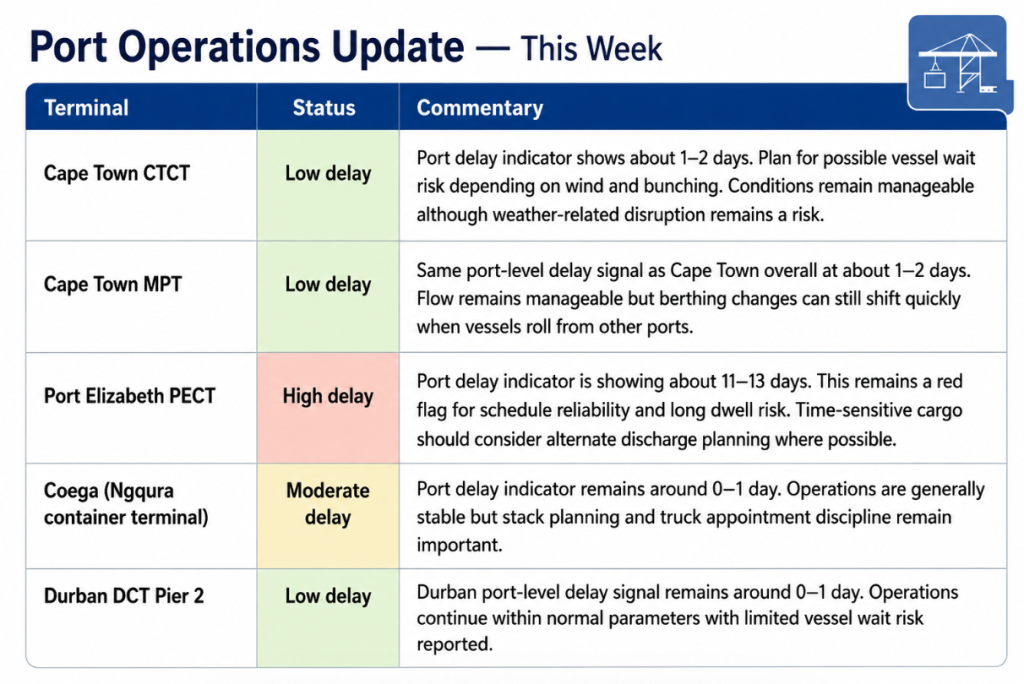

Port Operations Summary: – Port Update:

Severe weather warnings remain in place across multiple parts of South Africa this week, with heavy rain, strong winds and disruptive conditions expected to impact inland transport and port operations. As winter conditions begin to develop operational pressure is expected to increase, particularly around Cape Town and coastal corridors where weather-related delays can shift quickly.

Key Highlights from Last Week’s Discussions – 3 May 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port performance improved this week, with container volumes increasing despite public holidays and ongoing operational constraints.

- Total container volumes increased by approximately 7% week on week to 45,804 TEUs

- An average of 6,543 TEUs handled per day, with higher volumes projected for the coming week

- Durban Pier 1 volumes increased significantly, although roadside congestion and RTG breakdowns impacted truck turnaround times

- Cape Town volumes declined due to reduced vessel activity and public holidays, but no major operational disruptions were reported

- Ngqura volumes increased following the return of berth D100 from maintenance

- Rail cargo out of Durban declined sharply by approximately 30% week on week to 1,556 containers

Key Insight: Port operations remain stable overall, but pressure is increasing on inland execution and truck movement, particularly in Durban where equipment and system issues are impacting flow.

Air Cargo

Airfreight volumes softened this week, particularly on outbound cargo.

- Total international air cargo volumes through ORTIA decreased by approximately 7% week on week to 6,070 tons

- Inbound cargo increased marginally by approximately 1% while outbound cargo declined by approximately 18%

- Global air cargo demand remains mixed, with elevated jet fuel prices continuing to support higher rates

- Global spot rates increased further to approximately $3.76/kg

Key Insight: Airfreight demand remains uneven, but pricing pressure continues due to fuel costs and ongoing global capacity constraints

Road and Border Crossings

Cross-border performance deteriorated again this week, with queue and transit times increasing across key corridors.

- South African border crossing times averaged approximately 8.7 hours, improving slightly week on week

- SADC regional border crossings increased to approximately 7.6 hours, up 17% week on week

- Total indirect delay costs increased to approximately R747 million for the week

- Significant congestion continued at Groblersbrug and Kazungula, with operational and infrastructure constraints impacting flow

Protest action on the N3 near Heidelberg created additional transport disruption risk during the week

Key Insight: Border and corridor delays remain a major operational and cost risk, with inland execution becoming increasingly difficult across regional supply chains.

Ocean Freight and Global Shipping

Global shipping remains constrained by geopolitical disruption and elevated operating costs.

- Strait of Hormuz disruption continues to affect approximately 650,000 TEU of weekly Persian Gulf traffic

- Vessel movements through the region remain approximately 90% below normal levels

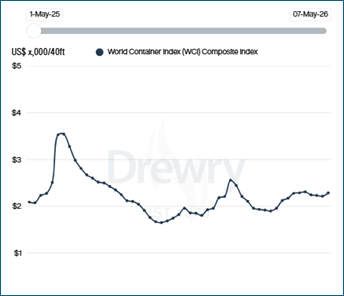

- Freight rates increased by approximately 3% week on week, with Drewry’s WCI rising to around $2,286 per 40ft container

- Schedule reliability improved by approximately 3.9% despite ongoing disruption

- Global containership orderbooks reached a record 13 million TEU, increasing long-term overcapacity concerns

Key Insight: The market remains operationally stable but highly constrained, with carriers managing disruption through rerouting, diversions, and controlled capacity rather than widespread service collapse.

Strategic Outlook

Operations remain stable locally, but pressure continues shifting toward inland execution, border reliability, and fuel-driven cost escalation. Businesses should focus on planning, transport coordination and managing exposure to routing and energy-related volatility. The key risk is no longer only at port level, but across the full supply chain from origin to final delivery.

Global Freight Rates

Drewry’s World Container Index increased slightly this week to approximately $2,286 per 40ft container, confirming that freight rates remain relatively stable but continue to be supported by operating costs rather than strong demand growth. The market remains balanced, with carriers maintaining pricing discipline as fuel and geopolitical pressures persist.

On the Asia – Europe trade, rates remained relatively stable this week, with carriers continuing to manage capacity and protect pricing levels despite softer global demand conditions. The market remains operationally stable, although upward movement remains limited by available capacity across major trade lanes.

On the Transpacific trade, rates also remained firm, supported by controlled supply and stable cargo flow. While demand is not showing significant growth, carriers continue to manage vessel deployment and sailing schedules to support rate stability.

The impact of the Middle East situation remains visible through higher bunker fuel costs and ongoing operational risk rather than direct disruption to South Africa’s primary trade lanes. Elevated fuel costs continue to support freight pricing globally, while uncertainty around routing and vessel security remains a concern across the market.

Overall, the market remains stable from a capacity perspective but constrained by cost pressure and geopolitical uncertainty. Freight rates are holding at elevated levels, with pricing expected to remain driven by fuel costs and carrier capacity management rather than a meaningful increase in demand.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”