Welcome to another Logistics News Update.

As we reach the end of the month, planned protest action across South Africa has caused a sharp slowdown in logistics activity, many transporters and businesses have chosen to limit cargo movements rather than place drivers, vehicles, and valuable cargo at unnecessary risk.

While the full extent of the disruption is still developing, the impact is already being felt through delayed collections, reduced deliveries and increased pressure on movements that must proceed. The immediate priority is safety, but the disruption also highlights how quickly supply chains can be affected when road access and operating conditions become uncertain. Businesses with urgent cargo should remain in close contact with their logistics providers and allow additional time for collections and deliveries as operations return to normal.

Also, important this week is the decision by SABS and the Department of Trade, Industry and Competition to place the proposed PVoC programme on hold while further consultation takes place. The programme was due to become mandatory on 20 September 2026. Importers should not assume that the requirement has disappeared permanently. This is an opportunity to engage suppliers, review tariff classifications and prepare the required product information so that the business is ready if a revised programme is introduced.

Another development requiring close attention is the introduction of mandatory driver inductions at Durban Container Terminal Pier 1 from 1 July. Drivers collecting or delivering containers will need to complete the induction process and provide the required supporting documents before entering the terminal. Industry has warned that manual verification could create additional queues and slower truck turnaround times during the initial rollout. There may be delays while the new process settles and clients should allow additional time for collections and deliveries. Please remain patient with transporters and service providers while they manage the additional terminal requirements.

Agri & Transport Summary

South Africa’s citrus export outlook strengthened further this week after the 2026 lemon export estimate was revised upward by 3.6 million cartons. The Citrus Growers’ Association increased its forecast from 45.8 million to 49.4 million 15kg cartons following favourable growing conditions across key production regions. The additional volume is positive for growers and exporters, but it will place further pressure on the citrus logistics chain during the remainder of the season. Packing remains concentrated in areas including Senwes, Patensie and the Boland while the largest upward revisions were recorded in Letsitele and the Sundays River Valley. The season is also expected to end more abruptly than usual with volumes forecast to fall sharply around mid-July rather than reduce gradually.

This creates a narrower and more intense transport window. Exporters will need strong coordination between farms, packhouses, cold stores, transporters and ports to avoid congestion, missed vessel cut offs and unnecessary storage costs. Further pressure is developing on the input side. Global fertiliser trade fell by almost 30% during the first four months of 2026 while the FAO fertiliser basket price increased from approximately US$475 per tonne in February to about US$595 per tonne in May. Conflict related disruption in the Gulf and export restrictions remain important risks for fertiliser availability and future farming costs.

What to monitor: Citrus transport and port capacity as lemon volumes increase and any further movement in fertiliser availability and pricing ahead of the 2026/27 summer crop season.

Logistics & Trade Headlines

- PVoC implementation has been placed on hold: SABS and the Department of Trade, Industry and Competition have stopped all implementation and readiness activities linked to the proposed Pre Export Verification of Conformity programme while further consultation takes place. The requirement was due to become mandatory on 20 September 2026, but no implementation action will proceed until a further decision is made. Importers should treat this as temporary relief rather than a permanent cancellation.

- New Durban port driver checks may create gate delays: Mandatory driver inductions are due to begin in July for drivers collecting or delivering containers at Durban Container Terminal Pier 1 and the Durban Multi-Purpose Terminal. Industry has warned that manual document checks could increase queues, turnaround times, and transport costs. Transporters should ensure that driver documentation is prepared before implementation begins.

- Far East shipping surcharges will increase landed costs: Maersk will introduce Peak Season Surcharges of US$250 per 20-foot container and US$500 per 40-foot container from 1 July while CMA CGM has introduced charges of between US$400 and US$550 per TEU from 21 June. The surcharges apply to cargo moving from the Far East to South Africa, Mauritius and Mozambique and should be included in landed cost calculations.

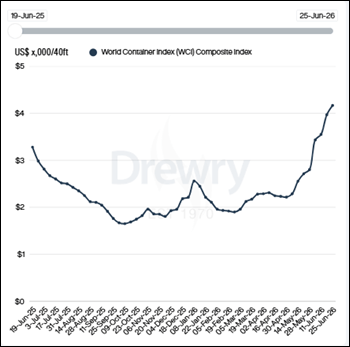

- Global container freight rates have increased again: Drewry’s World Container Index rose by a further 5% to US$4 166 per 40-foot container on 25 June which was its highest level since September 2024. The increase was driven mainly by continued pressure on the Transpacific trade while limited blank sailings indicate that carriers are maintaining most scheduled capacity.

- Cape Town Container Terminal is adding hybrid equipment: Four new hybrid straddle carriers are expected to enter service in July following a R96 million investment by Transnet Port Terminals. The equipment is intended to improve yard capacity and give the terminal greater flexibility in managing container movements although weather disruption will remain an important operational risk.

- Transnet is looking for a private partner for freight rail equipment: Transnet is seeking a private sector partner to establish a rolling stock leasing company that would improve access to locomotives and wagons for freight rail operators. The initiative could support greater private participation in rail, but its value will depend on execution, equipment availability and whether sufficient freight volumes move from road to rail.

What to monitor: The practical effect of the new Durban driver checks, further shipping surcharge announcements, any revised PVoC timetable and whether rising international freight rates begin affecting South African import pricing more materially.

Let’s Learn, what is a Peak Season Surcharge and why does it matter?

A Peak Season Surcharge is an additional charge applied by a shipping line when demand, capacity pressure or operating conditions increase the cost or difficulty of moving cargo on a particular trade route. Despite the name, the charge is not always limited to a traditional seasonal peak. It may also be introduced when cargo demand rises quickly, vessel space becomes tight or carriers face higher operating costs.

In practical terms:

The surcharge is added on top of the base ocean freight rate and normally applies to specified origins, destinations, container types, and shipment dates. It may be charged per container or per TEU. A 40-foot container is generally treated as two TEUs which means a charge quoted per TEU can have a larger effect on a 40-foot shipment than an importer initially expects. The effective date is also important. Depending on the carrier and contract, the surcharge may apply according to the booking date, price calculation date, vessel departure date, or cargo loading date.

Where people get caught:

• A freight rate is accepted before the surcharge is announced but the shipment moves after the effective date

• The surcharge is quoted per TEU rather than per container

• The original quote expires before the cargo is ready

• The supplier delays production and the shipment moves under a new rate period

• The importer compares base freight rates without comparing the applicable surcharges

• The surcharge applies only to certain origins, destinations, or container types

• The landed cost is approved without allowing for possible rate changes before shipment

Quick example:

An importer receives a base freight rate of +/-US$2 000 for a 40-foot container from China to South Africa, before the container is loaded, the carrier introduces a Peak Season Surcharge of +/-US$500 per 40-foot container. The ocean freight cost is now around US$2 500 before any additional local charges, customs costs or inland transport are added. If the surcharge is quoted at US$400 per TEU, the additional cost on a 40-foot container could instead be US$800.

What importers should check

Before approving a shipment, confirm:

• The validity period of the freight rate

• Whether the rate includes all current carrier surcharges

• The date that determines whether a new surcharge applies

• Whether the charge is per container or per TEU

• Whether the cargo is likely to move before the rate expires

• Whether the landed cost includes a reasonable allowance for rate movement

Takeaway:

A Peak Season Surcharge does not necessarily mean that the original quote was incorrect. It means that the commercial conditions applying to the shipment changed before the cargo moved. Importers should therefore avoid treating an early freight estimate as a fixed final cost unless the rate, surcharge exposure and shipment timing have all been confirmed.

NEWS

N3 Upgrade Brings Long Term Capacity but Five Years of Disruption

Freight News

Construction has started on SANRAL’s R6 billion upgrade of the N3 between the Mariannhill Toll Plaza and Key Ridge in KwaZulu Natal. The project is expected to improve long term road capacity and safety, but motorists and freight operators have been warned to expect significant traffic disruption over the next five years. The N3 is one of South Africa’s busiest freight corridors and carries a large volume of cargo between the Port of Durban, KwaZulu Natal and the Gauteng market. Any reduction in lane capacity, temporary diversions or construction related congestion can therefore affect truck turnaround times, delivery schedules, and transport costs.

The upgrade is necessary because the route has been operating under growing pressure from increasing freight and passenger traffic. However, the commercial risk during construction will be the cumulative effect of slower movements, unpredictable delays and additional operating time for transporters using the corridor. Importers and exporters should not treat this as a once off roadworks issue. Transport planning may need to allow additional transit time throughout the project while urgent and time sensitive cargo may require earlier collection, revised delivery windows, or alternative staging arrangements.

The long-term benefit should be a safer and more efficient corridor, but the next five years will require closer planning and communication between cargo owners, transporters, warehouses, and delivery sites. What to monitor: Lane closures, traffic diversions, and construction schedules along the Mariannhill to Key Ridge section of the N3 together with any effect on Durban to Gauteng transit times.

Source: Adapted from Freight News

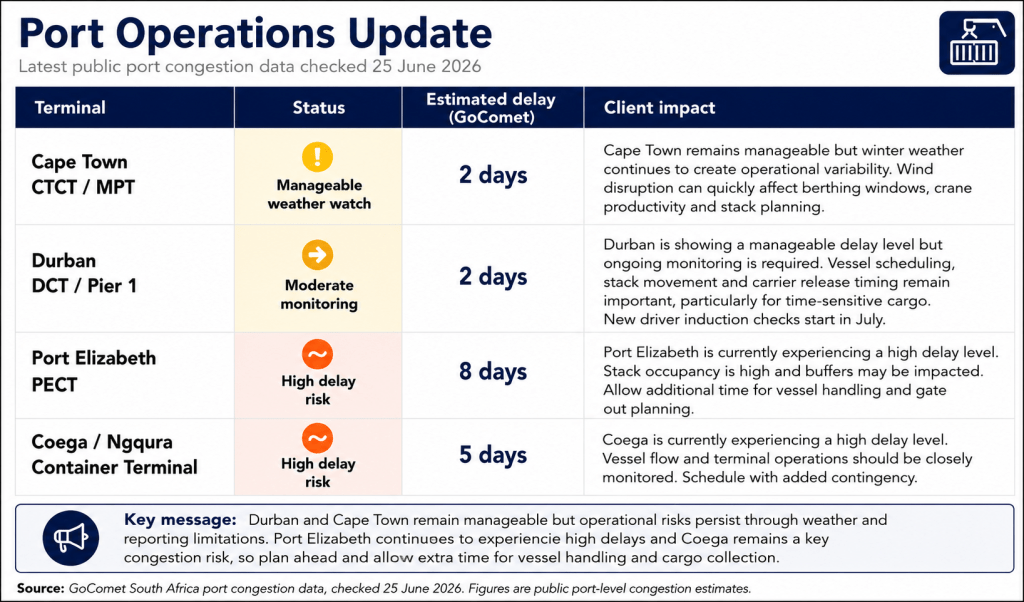

Port Operations Update:

South African port operations remain active, but conditions are still uneven across the main container terminals. Current GoComet data shows relatively manageable delays at Durban, Cape Town, and Port Elizabeth while Coega remains the main congestion concern. Recent weather-related backlogs and tidal restrictions in the Eastern Cape mean that conditions can change quickly and individual vessel schedules should still be checked before delivery commitments are confirmed.

- Durban: Current public congestion data reflects a delay of approximately two days. Operations remain manageable but the planned introduction of mandatory driver inductions at Pier 1 and the Durban Multi-Purpose Terminal from July could place additional pressure on terminal gates and truck turnaround times. Transporters should ensure that driver documentation is complete before the new process begins.

- Cape Town: Current congestion is approximately one day. The port remains operational and four new hybrid straddle carriers are expected to enter service during July which should support yard capacity and terminal flexibility. Wind remains the main operational risk and can quickly affect vessel working and berthing schedules.

- Coega and Ngqura: Current GoComet data reflects a delay of approximately five days which makes this the main port to monitor this week. Recent operational reporting identified seasonal tidal restrictions and backlogs following adverse weather as factors affecting productivity and cargo flow. Exporters should allow additional flexibility around vessel cut offs and cold chain planning.

- Port Elizabeth: Current GoComet data reflects a delay of approximately one day. However, recent weekly reporting recorded vessel waiting times of around 8.5 days during a period of weather disruption and Eastern Cape backlogs. This difference shows how quickly conditions can change and why shipment specific schedules should be checked rather than relying only on a general port average.

What to monitor: Congestion at Coega, possible gate delays linked to the new Durban driver requirements and any further wind or weather disruption affecting Cape Town and the Eastern Cape ports.

Key Highlights from Last Week’s Discussions – 14 June 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

South African container terminals handled 65 621 TEUs during the week of 15 to 21 June which was 7% higher than the 61 252 TEUs handled during the previous period. The daily average increased to 9 374 TEUs and was 20% above the projected average of 7 809 TEUs. Cape Town Container Terminal recorded the strongest large terminal improvement with weekly volumes increasing by 25% to 18 534 TEUs. Port Elizabeth increased by 52% to 8 054 TEUs while Durban Pier 1 improved by 13% to 17 299 TEUs. Ngqura remained broadly stable at 19 301 TEUs which was 1% lower than the previous week. Formal throughput information for Durban Gateway Terminal remains unavailable following the transition from Durban Container Terminal although separate operational reporting indicated that DGT throughput decreased slightly by 2% to approximately 2 606 containers per day. Operational performance remained uneven. Cape Town maintained strong waterside performance despite weather disruption while Port Elizabeth vessels waited an average of 108 hours at anchorage before berthing. Durban Pier 1 truck turnaround time increased by 43% to approximately 60 minutes and staging time increased by 46% to approximately 35 minutes.

Key Insight: Port throughput improved strongly overall but higher volumes did not remove operational risk. Anchorage delays in the Eastern Cape, longer truck turnaround times in Durban and incomplete DGT reporting continue to affect planning visibility.

Air Cargo

International air cargo through OR Tambo increased by 6% week on week to approximately 7 391 tonnes. Inbound cargo increased by 5% to approximately 4 681 tonnes while outbound cargo increased by 8% to approximately 2 710 tonnes. Current international air cargo volumes were 18% higher than June 2025 and 16% above June 2019 levels. Global air cargo conditions remained stable with worldwide tonnage increasing by 1% while capacity and average rates were unchanged. Average global pricing remained at approximately US$3.23 per kilogram and was still around one third higher than the same period last year.

Key Insight: Air cargo demand remains firm and South African volumes continue to perform above both last year and pre pandemic levels. Pricing has stabilised week on week but remains materially higher than a year ago.

Road and Border Crossings

Average South African border crossing times improved by 4% to approximately 7.8 hours. In contrast average crossing times across the wider SADC region increased by 15% to approximately 8.2 hours. Lebombo truck volumes increased by 6% to approximately 1 545 heavy vehicles per day. Queue times remained stable at approximately 4.7 hours while processing times averaged approximately 4.4 hours per crossing. Kasumbalesa remained the most constrained crossing with transit from the Zambian side taking approximately six days. Chirundu and Katima Mulilo also recorded average crossing times of more than one day. The total indirect cost of cross border delays increased by 15% to an estimated R812 million. Queue delays accounted for approximately R434 million while excess border transit time contributed a further estimated R379 million.

Key Insight: South African border performance improved slightly but the regional picture deteriorated. The financial cost of cross border delays increased sharply which means corridor specific congestion remains more important than the overall regional average.

Ocean Freight and Global Shipping

Container freight markets remained firm with carriers preparing further July rate increases of as much as US$5 000 per 40-foot container on certain routes. Cargo demand is now reported to be exceeding available vessel slots while port congestion continues to remove effective capacity from the market. Global containership capacity waiting at anchorages increased to approximately 3.4 million TEUs. Conditions around the Strait of Hormuz remain uncertain despite the peace agreement signed on 17 June. Only nine container ships had departed the Persian Gulf while more than 50 remained stranded because of uncertainty over transit terms. The report also warned that published vessel delay figures may understate actual disruption because carriers are adding more buffer time to schedules. This can improve reported schedule reliability without necessarily improving the underlying transit time experienced by cargo owners.

Key Insight: Freight rate pressure remains elevated and published schedule performance may not reflect the full level of disruption. Importers should assess actual transit time, available vessel space, and applicable surcharges rather than relying only on headline schedule reliability.ons are improving operationally in some areas, but freight rates and geopolitical risk remain material cost drivers.

Strategic Outlook

The week showed stronger port and air cargo volumes with improved performance at Cape Town, Durban Pier 1 and Port Elizabeth. However, the system remains uneven. Eastern Cape anchorage delays, rising Durban truck turnaround times, cross border congestion and further global freight rate increases remain material risks. Businesses should continue reviewing each shipment against current port, border, and carrier conditions because stronger headline volumes do not necessarily mean more reliable or lower cost execution.

Global Freight Rates

Drewry’s World Container Index increased by a further 5% to US$4 166 per 40-foot container on 25 June. This was the highest level recorded since September 2024 and followed the 12% increase reported the previous week. The index has now risen by approximately 17% over the two latest reporting periods.

The latest increase was driven mainly by continued strength on the Transpacific trade. Shanghai to New York increased by 6% to US$7 149 per 40-foot container while Shanghai to Los Angeles rose by 12% to US$5 750. Drewry reported that only four blank sailings had been announced on the Transpacific trade for the following week which indicates that strong demand rather than aggressive capacity withdrawal is supporting the latest rate movement.

Asia to Europe rates were comparatively stable. Shanghai to Rotterdam increased by 1% to US$4 392 per 40-foot container while Shanghai to Genoa remained unchanged at US$5 759. Only three blank sailings were announced on the Asia to Europe trade for the following week which continues to indicate constrained available capacity.

The latest movement confirms that freight pricing remains firm despite relatively limited blank sailings across the main east west routes. Strong cargo demand, frontloading, and tight vessel availability continue to support rates while port congestion removes effective capacity from the market. Drewry reported that only 24 blank sailings are expected across the major east west trades over the next five weeks which represents a cancellation rate of approximately 3%.

Importers should not assume that earlier freight rates or landed costs will remain valid. Rate validity, carrier space, Peak Season Surcharges, fuel related charges and booking deadlines should all be confirmed before commercial commitments are made.

What to monitor: Whether carriers are able to implement the additional July rate increases and whether strong demand continues to support the latest pricing despite scheduled capacity remaining broadly available. Source: Drewrey World

Final Thoughts

This week’s update shows that South Africa’s logistics network is moving more cargo but remains exposed to disruption, rising costs, and uneven operating conditions. Port and air cargo volumes improved while freight rates continued to increase and cross border delay costs moved higher. The immediate concern is the planned protest action on 30 June. Although government has confirmed that it remains a normal working day and not an official national shutdown, approved marches, road closures, and possible localised disruption create a genuine risk for drivers, vehicles, and cargo. Many transporters and cargo owners have therefore taken a cautious approach by reducing non-essential movements and completing urgent collections and deliveries before the day. This may slow logistics activity temporarily but protecting people, vehicles and valuable cargo must remain the priority.

Businesses should remain in close contact with their transporters and logistics providers and avoid assuming that normal lead times will apply. Where movements cannot be postponed, additional time should be allowed, and alternative routing should be considered where practical. The broader market also requires careful cost control. Freight rates remain firm, carrier surcharges are increasing and border delays continue to create significant indirect costs. The strongest protection remains confirming every shipment detail before the cargo moves.

• Operational: Confirm driver availability, planned routes, road closures, port access, and delivery arrangements before dispatching cargo on 30 June.

• Safety and risk: Avoid unnecessary movements where possible and do not place drivers, staff, or cargo at risk to meet a delivery window.

• Market and cost: Reconfirm freight validity, carrier space, and surcharge exposure before finalising landed costs.

• Planning: Expect some congestion and delayed collections after 30 June as postponed movements return to the network.

The logistics environment remains operational but tomorrow should be approached with caution, good planning may delay a shipment by a day while poor planning can expose a business to far greater cost and risk.

Disclaimer:The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade™ 360 — your partner in logistics and Exporters Western Cape