Welcome to another Logistics News Update.

As we move into May, the final month of autumn in South Africa, cost pressure continues to build. An orange weather warning for Gqeberha on the 6th adds further risk, with potential impact on port operations and delivery timelines. Electricity & logistics tariffs increased from 1 April, fuel remains volatile and any upward move flows straight into transport, distribution, and inland delivery costs. The South Africa Government’s relief on the fuel levy has been extended into May, which is helping to cushion the increase, but it does not remove the risk, it only slows the impact.

The logistics system is operating but the pressure is shifting, the risk is moving away from port congestion and toward cost, border delays, and reduced visibility. In this environment, planning earlier, tightening execution, and maintaining control across the full supply chain is what separates a clean delivery from avoidable leakage through delays, storage, detention and missed slots.

Newsworthy: South Africa to crack down on dodgy imports: Government is moving to tighten controls on substandard and unregulated imports, starting with key trading partners like China. A new pre-export verification programme will require certain goods to meet South African safety and quality standards before shipment, with wider rollout expected to other countries. Authorities are responding to a surge in unsafe and non-compliant goods entering the market, estimated to make up a significant portion of consumer products. The aim is to protect consumers and local manufacturers while improving compliance across the import value chain.

Agri & Transport Summary

South Africa’s agricultural export season continues to build, particularly in citrus, with volumes increasing through the supply chain. The Middle East remains a key but uncertain market, and exporters are applying caution when committing cargo into the region. The risk is centred around timing and reliability, with ongoing geopolitical tension creating variability in routing and delivery conditions.

From a logistics perspective, the system remains stable. Durban continues to operate efficiently, while Cape Town remains weather sensitive but within normal parameters. As volumes increase, the pressure is shifting toward execution, where delays in transport, documentation or coordination can impact delivery performance. Cost remains the primary constraint. With the majority of agricultural exports moving inland by road, fuel prices continue to drive transport costs and margin pressure. The focus remains on maintaining consistency and managing exposure to both cost and market risk.

Logistics & Trade Headlines

- Fuel pressure remains elevated: Oil prices continue to trade at high and volatile levels, supporting elevated diesel costs and ongoing pressure on transport and logistics pricing. There is no confirmed sustained easing at this stage.

- Geopolitical risk remains unresolved: Tensions in the Middle East continue with no clear signs of de-escalation, maintaining pressure on energy markets and overall supply chain risk.

- Strait of Hormuz remains operational: Vessel movement continues with no confirmed closure, but the region remains high risk with ongoing security concerns and potential for disruption.

- Citrus exports continue to grow: SA’s citrus export volumes are expected to increase this season as new orchards come into production and demand remains stable across key markets. The main pressure remains on cost, with higher fuel and inland transport costs impacting margins as volumes increase.

- Middle East uncertainty impacting export decisions: The region remains a key market, but conditions are becoming more uncertain, with ongoing geopolitical tension affecting routing, timing and reliability. Exporters are showing more caution when committing cargo due to the increased risk of delays.

- No direct disruption to South Africa’s main trade lanes: Asia to South Africa container routes remain operational, with the impact continuing to be indirect through cost and insurance rather than physical delays.

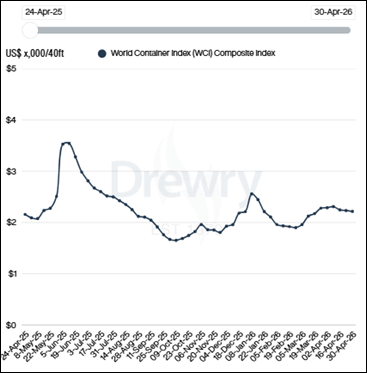

- Freight rates remain elevated: Drewry’s World Container Index continues to trade in the range of approximately $2,200 to $2,300 per 40ft container, indicating a stable market supported by cost rather than demand growth.

- Bunker costs remain a key driver: Elevated fuel costs continue to support freight rates, with carriers maintaining pricing discipline across major trade lanes.

- Airfreight demand remains soft: Global volumes are flat to slightly down, while rates remain supported by fuel costs and operational constraints.

- Port performance remains stable: South African ports continue to operate within normal parameters, with no widespread congestion reported.

- Durban and Cape Town operating within normal ranges: Vessel queues remain stable, although Cape Town remains sensitive to intermittent weather-related disruption.

- Rail performance remains under pressure: Ongoing rail constraints continue to shift cargo onto road, increasing exposure to higher transport costs.

- Border conditions remain mixed: South African border crossing times remain slightly elevated, while regional SADC crossings continue to show variability, highlighting ongoing structural inefficiencies.

Let’s Learn – Incoterms decide cost, control, and when risk shifts

Incoterms are the trade terms on your invoice that decide who arranges transport, who pays which charges and when the risk transfers from seller to buyer, they look like a small detail, but they often explain surprise costs, delays, and claim disputes.

In practical terms:

The Incoterm guides your forwarder and clearing agent on who books main carriage, who insures the cargo, who handles export and import formalities, and who has authority to instruct the carrier.

Where people get caught:

- Freight, insurance, and local charges were not budgeted for, so landed cost and margin are wrong

- Responsibilities are unclear, so documents, releases, or bookings get stuck

- Insurance is assumed, then a loss happens, and the cover is inadequate

Quick example:

CIF can look cheaper because the supplier gives you one number that includes ocean freight and insurance to the destination port but that freight line often carries supplier margin and you usually have less control over routing, service levels and insurance quality, you also still pay destination charges, clearance and delivery inland, so the landed cost can end up higher than expected.

Takeaway:

Confirm the Incoterm before booking, make sure it matches the purchase order and commercial invoice, then align it with your clearing and forwarding instructions, because clarity upfront prevents cost and delay later.

NEWS

Freight rates on steep conflict curve

Sea freight spot rates are staying elevated as conflict driven disruption keeps the market jittery, with key North Europe and Mediterranean routes sitting about 15 percent above the October dip when demand was at a six-month low, which tells you the floor has lifted, and shippers should plan for ongoing volatility rather than a quick correction.

On the North Europe lane, rates on 29 April were quoted at about US$2 668 per FEU, roughly 8 percent higher than levels before 28 February when the Iran conflict escalated and the Strait of Hormuz became a pressure point in the supply chain, Mediterranean rates were around US$3 527 per FEU which is slightly below late February levels, and carriers such as Maersk are using blank sailings again to pull capacity out and hold rates up.

Across the Transpacific, the pressure is showing clearly, West Coast rates are up to about US$2 675 per FEU which is 45 percent higher since the Persian Gulf disruptions began, East Coast rates are sitting close to US$4 000 per FEU, and with Gulf region container flows being rerouted through alternative corridors there are reports of congestion and uneven equipment availability, with additional services being pushed through hubs like Jeddah to relieve bottlenecks.

Air freight is also running hot, with rates about 30 percent above pre conflict levels as jet fuel costs rise and short haul capacity cuts from Lufthansa and KLM tighten supply, United has added cargo surcharges and some South East Asia long haul routings now require extra refuelling stops which pushes costs up further, capacity is slightly below pre conflict levels but the Freightos Air Index shows pricing holding steady, with China to North America at about $6.40 per kilogram, China to Europe at $5.07 per kilogram and South Asia to Europe at $4.94 per kilogram while South East Asia to Europe has edged up but remains below recent peak

Source: Adapted from FreightNews

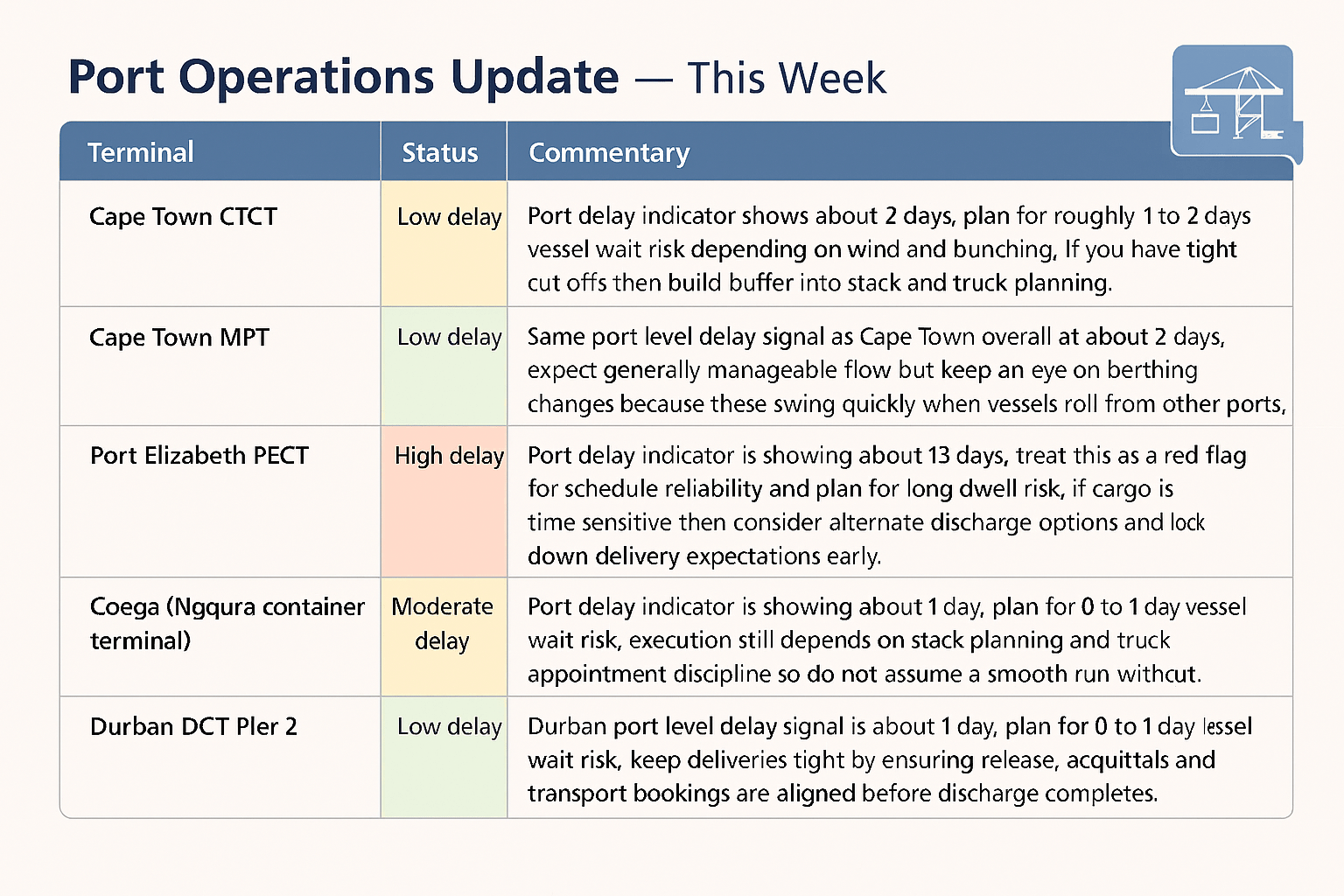

Port Operations Summary: – Port Update:

Quick operational note

These are port level delay indicators and individual terminal conditions can differ on the day, so the right move is to treat Port Elizabeth as the current risk point, then manage Cape Town and Durban as controllable with proper planning and treat Coega as moderate risk where small execution gaps become demurrage and storage quickly.

Key Highlights from Last Week’s Discussions – 26th April 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port performance remains stable with a slight decline in volumes.

- Total container volumes decreased by approximately 3% week on week to 42,985 TEUs

- Cape Town and Durban operated without major disruptions, with lower volumes linked to public holidays and reduced vessel activity

- Eastern Cape volumes declined due to weather conditions and berth maintenance constraints

- Rail volumes out of Durban decreased by approximately 12% week on week

Key Insight: Ports remain stable with no congestion risk. Volume changes are timing related, not operational weakness.

Air Cargo

Airfreight volumes increased, showing early signs of recovery.

• Total volumes increased by approximately 9% week on week to 6,806 tons

• Growth driven by inbound recovery and post-holiday demand

• Global rates remain elevated at around $3.70/kg despite improving capacity

• Capacity is improving, particularly from the Middle East and South Asia

Key Insight: Airfreight is stabilising, but rates remain elevated due to ongoing geopolitical and capacity constraints.

Road and Border Crossings

Cross-border conditions deteriorated, increasing delays and cost pressure.

• South African border crossing times increased to approximately 9.5 hours (up 19%)

• SADC crossings increased to approximately 6.5 hours (up 7%)

• Total indirect delay cost estimated at approximately R670 million for the week (up 13%)

• Severe congestion reported at key borders, with Groblersbrug delays reaching up to 10 days

Key Insight: Border performance is deteriorating. Delays are becoming structural and are now a key driver of cost and reliability risk.

Ocean Freight and Global Shipping

Global shipping remains constrained by geopolitical and energy pressures.

• Strait of Hormuz disruption continues to impact approximately 25% of global crude oil trade

• Vessel traffic has improved slightly, but flows remain 90–95% below normal levels

• Global freight rates softened marginally to around $2,232 per 40ft (down 0.6%)

• Carriers are slowing vessels to manage fuel costs, increasing transit times

• Schedule reliability improved to approximately 62.2%

Key Insight: The system remains stable but constrained. Cost pressure is being driven by fuel, routing inefficiencies, and managed capacity.

Strategic Outlook

Operations remain stable locally, but pressure is shifting into cost, border delays, and global energy risk. Businesses should focus on planning, managing inland execution, and controlling exposure to fuel and routing changes. The risk is no longer just delays at port; it is execution across the full supply chain.

Global Freight Rates

Drewry’s World Container Index softened again this week, decreasing slightly to approximately $2,232 per 40ft container. This confirms that rates remain elevated but are under mild downward pressure, with the market being supported by cost rather than demand growth. On the Asia – Europe trade, rates declined, with Shanghai to Genoa down around 8% and Shanghai to Rotterdam down around 4%. This reflects excess capacity and limited blank sailings, with carriers unable to push rates higher despite ongoing cost pressure. On the Transpacific trade, rates edged slightly higher as carriers continue to manage capacity. Demand remains stable but not strong, with pricing supported more by controlled supply than underlying growth.

On the Transatlantic trade, rates increased sharply by approximately 15%, driven by capacity reductions and peak season surcharges. This shows that carriers are still actively managing lanes where they can protect margin. The impact of the Middle East situation remains structural. The Strait of Hormuz disruption continues to affect global energy markets, with bunker fuel costs elevated and vessel speeds reduced as carriers manage fuel consumption. This is extending transit times and reducing effective capacity across trade lanes.

Overall, the market remains stable from a capacity perspective but constrained by cost and network inefficiencies. Freight rates are not accelerating, but they are not collapsing either. In the short term, pricing will continue to be driven by fuel costs, carrier capacity management, and geopolitical developments rather than any meaningful demand recovery.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”