Welcome to another Logistics News Update.

With the conflict involving Iran dominating global headlines, many importers and exporters are asking what this means for logistics and whether supply chains will be disrupted. In shipping the first question is always route exposure. Not every conflict immediately affects global container trade.

From a South African perspective, the direct impact on our main Far East trade lanes remains limited at this stage. Most cargo moving between Asia and South Africa does not transit the Persian Gulf or the Strait of Hormuz. This means the immediate risk is not route disruption but rising global transport costs.

What we are seeing instead is an increase in global risk costs. Shipping lines are becoming more cautious around the Gulf region, insurance costs for vessels have increased and war risk premiums are being introduced. In some cases, vessels are adjusting routes to avoid higher risk areas. This results in longer sailing distances, higher fuel consumption, and higher insurance costs. As we often see in shipping, geopolitical instability quickly translates into higher freight pricing across global trade lanes, even where routes are not directly affected.

For South Africa, the bigger risk is energy. Around 20 percent of the world’s oil supply moves through the Strait of Hormuz. Any disruption in that region places upward pressure on oil prices. When oil rises bunker fuel costs increase, aviation fuel increases and transport costs rise across the entire supply chain.

The result is predictable. Ocean freight rates begin to increase; air freight becomes more expensive, and trucking costs rise locally. Fuel affects almost every part of the South African economy and historically we see these cost pressures begin filtering through within two to six weeks. This is often accompanied by emergency surcharges from carriers.

For exporters, particularly in the fruit and agricultural sectors, the risks are slightly different. The key concerns are higher freight costs, potential disruption to Middle East markets and pressure on air freight capacity. These challenges may also coincide with the usual cost adjustments that come into effect on 1 April.

In simple terms the impact on South Africa is currently indirect and driven mainly by cost pressure rather than route disruption.

The main risks to monitor are:

1. Higher oil prices (you going to pay more at the pumps and transporters will charge fuel levies as will the shipping lines in the form of BAF)

2. Rising bunker fuel costs (known as BAF Bunker Adjustment Factor basically a fuel levy for shipping lines)

3. Shipping line surcharges (known as a war surcharge or insurance surcharge for example)

4. Potential disruption to Middle East export markets (if you are exporting to this region, you will pay more and their will disruptions)

For now, the situation remains manageable, but as always in global logistics we will continue monitoring developments closely and advise clients as conditions evolve.

First Trade 360 offers its clients up to 90 days payment terms on logistics costs, including freight, duties, and VAT, helping businesses manage cash flow while keeping supply chains moving. If the current market conditions are placing pressure on your logistics costs, this facility can provide valuable flexibility. Should you require assistance or would like to understand how the facility works, please contact Kevin Pillay on 082 334 8101 or email kevin.pillay@fnb.co.za.

Agri Trade Advisory: Foot and Mouth Disease and Export Risk:

South Africa continues to manage outbreaks of Foot and Mouth Disease (FMD), which remains an important issue for the agricultural sector and international trade. The most direct export impact to date has been on red meat products, where certain international markets have imposed restrictions following outbreaks. At this stage there is no confirmed blanket ban on South African wool exports linked to FMD, but animal disease status remains a key factor monitored by importing countries. For agricultural exporters, the main risks are not only potential market restrictions, but also the operational impact of disease control measures. Movement controls, biosecurity protocols and veterinary compliance requirements can influence how livestock and animal-derived products move through the supply chain.

From a logistics perspective, exporters should ensure that all health certification, traceability documentation, and export protocols are aligned with the requirements of destination markets, particularly when trading with sensitive agricultural markets. While the situation is being actively managed by authorities, the issue remains one to monitor closely as animal health status can influence trade access very quickly. For exporters, particularly in the livestock and agricultural sectors, maintaining clear traceability and health certification remains critical when accessing international markets.

Let’s Learn: Why Freight Rates Sometimes Increase Even When Routes Are Not Disrupted

Many importers assume freight rates only increase when a shipping route is physically disrupted. In reality, rates often rise even when vessels are still moving normally.

Why this happens:

Shipping costs are influenced by global risk and operating costs, not just the physical route. When geopolitical events occur several cost factors change immediately.

What drives rate increases:

• Fuel prices increase which raises bunker costs for vessels

• Insurance premiums rise for ships operating in higher risk regions

• Carriers introduce war risk or emergency surcharges

• Shipping lines reduce capacity to manage risk and protect schedules

Even if your cargo does not travel through the affected region, these cost increases are applied across global trade lanes.

Where importers and exporters feel the impact:

• Higher freight rates

• Additional surcharges

• Shorter validity periods on rate offers

• Increased volatility in pricing

Playbook:

Do not assume that a route must close before costs increase. In global logistics pricing often reacts to risk and operating costs long before physical disruption occurs.

Here is your weekly logistics news.

- Iran conflict beginning to affect global logistics networks: War-risk insurance increases, vessel delays in the Persian Gulf and airspace restrictions across the Middle East are starting to influence global shipping and air cargo networks.

- Airfreight capacity tightening after Gulf flight cancellations: Emirates and Qatar flight disruptions reduced air cargo volumes through OR Tambo this week, highlighting the vulnerability of airfreight networks that rely on Middle East hubs.

- Cape route diversions increasing global transit times: Some container services are avoiding the Gulf and Middle East risk areas, which is extending voyage distances and reducing effective vessel capacity.

- Port volumes rebound after Chinese New Year slowdown: South African container throughput strongly increased week on week as shipping schedules begin normalising after the holiday period.

- Cape Town operations improving after earlier weather delays: Wind disruption eased during the week allowing the terminal to recover some operational momentum and reduce vessel backlogs.

- Durban activity increasing as vessels return: Pier 1 reported improved berth utilisation and higher volumes as global shipping schedules resume.

- Rail movements from Durban decline week on week: Rail cargo handled out of Durban fell significantly, reinforcing the ongoing reliance on road transport

- Regional border delays continue to increase: Cross-border processing times across SADC remain elevated, with some corridors experiencing significant delays and congestion.

- Global shipping risk shifting toward cost pressure: Rising oil prices, war-risk insurance premiums and longer sailing distances are now beginning to push freight costs higher.

- South Africa likely to feel indirect effects of Middle East conflict: The primary impact locally will be higher energy costs, freight inflation, and supply chain volatility rather than direct disruption to Far East container routes.

NEWS

Pain for the rand as oil price soars above $100 per barrel

27 Feb 2026 – FreightNews

The escalation of the conflict involving Iran is now starting to affect global markets, with oil prices climbing above the critical $100 per barrel level for the first time in several years. Brent crude recently reached around $107 per barrel, reflecting a sharp increase in global energy costs as markets react to supply risks in the Middle East. The surge in oil prices has already begun placing pressure on the South African rand, which weakened to around R16.85 to the US dollar, losing roughly 2% in a single trading session as investors moved toward safer assets.

The concern for global markets centres around the Strait of Hormuz, one of the most important energy shipping routes in the world. Approximately 20% of global oil supply moves through this narrow waterway, making it a critical chokepoint for energy trade. Any disruption or threat to vessel traffic in this region quickly pushes oil prices higher as traders anticipate supply shortages and increased risk to tanker movements.

For South Africa, the impact is likely to be indirect but significant. The country imports a large portion of its refined fuel and therefore remains highly exposed to global oil price movements. As oil prices rise, the cost of petrol, diesel, aviation fuel, and bunker fuel all increase, which feeds directly into the cost of transport, logistics and ultimately the price of goods moving through supply chains.

Higher oil prices also tend to weaken emerging market currencies like the rand because investors shift capital toward safer assets such as the US dollar during geopolitical crises. This combination of a weaker currency and higher oil prices amplifies the cost impact for South Africa since fuel is priced in dollars on the international market.

From a logistics perspective, the most immediate effect is cost pressure rather than physical disruption to shipping routes serving South Africa. While global energy markets react quickly to geopolitical tension, the real impact locally is likely to be higher fuel costs, rising freight rates and increased volatility in supply chain planning if elevated oil prices persist. Source: FreightNews

Port Operations Summary: – Port Update:

Durban 1.5 days

Cape Town 4.5 DaysPort Elizabeth 1 days

Coega 3 Days Source: Savino Del Bene S.A.

Please check with your service provider as reports differ

Key Highlights from Last Week’s Discussions – 1st March 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations

Port volumes increased strongly week on week as activity recovered after the Chinese New Year slowdown.

• Total container volumes increased around 21% week on week

• Cape Town operations improved after earlier weather delays, with better crane availability and reduced vessel backlog

• Durban Pier 1 saw increased berth occupancy and higher volumes

• Ngqura and Port Elizabeth both reported improved throughput with steady equipment availability

• Rail cargo out of Durban declined by around 20% week on week

Takeaway: Port volumes are recovering after the Chinese New Year slowdown. Operational conditions are improving, although rail movements remain inconsistent.

Air Cargo

Air cargo experienced pressure due to the conflict in the Middle East and disruption at key Gulf hubs.

• Total air cargo volumes down around 16% week on week

• Inbound volumes declined around 26% following flight cancellations

• Outbound cargo increased slightly around 3%

• Emirates and Qatar flight cancellations reduced available cargo capacity through major hubs

Takeaway:Airfreight capacity tightened due to Middle East disruptions and flight cancellations, placing upward pressure on rates and space availability.

Road and Border Crossings

Cross-border conditions across the region remain volatile with increasing delays.

• South African border crossing times increased to around 12.7 hours on average

• SADC regional crossing times increased to around 7.6 hours

• Beitbridge congestion worsened significantly with some crossings taking more than a day

• Average regional transit times increased by more than 2 hours week on week

Takeaway: Border processing delays remain one of the biggest structural risks to regional supply chains.

Ocean Freight and Global Shipping

The escalation of the Iran conflict is beginning to influence global shipping markets.

• Around 147 vessels are currently waiting or idling in the Persian Gulf

• Approximately 650,000 TEU of container traffic linked to Gulf ports could be affected

• Some container services are rerouting via the Cape of Good Hope

• War-risk insurance withdrawals and rising premiums are increasing shipping costs

Takeaway:The main impact is rising costs and longer transit times rather than immediate disruption to container flows. South Africa may see increased vessel traffic around the Cape, but the larger effect will be higher freight and energy costs.

Global Freight Rates

Global Freight Rates

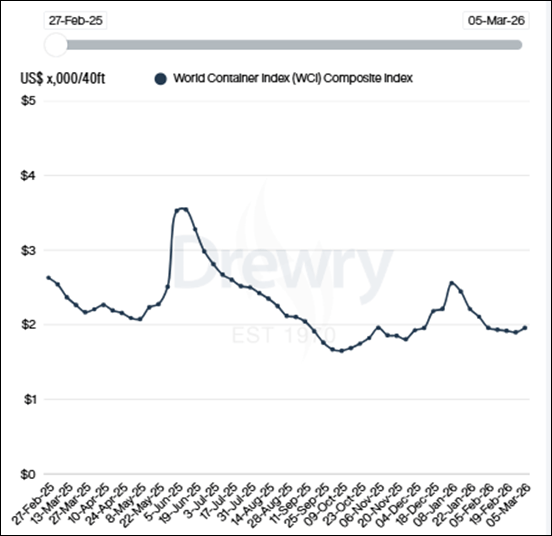

Weekly Container Rate Update – 5th March 2026

Drewry’s World Container Index increased 3% this week to $1,958 per 40ft container, driven largely by rate increases on the Transpacific trade lanes.

Rates on the Asia–Europe trade remain under pressure. Shanghai to Rotterdam declined 2% to $2,052, while Shanghai to Genoa increased only 1% to $2,844 per 40ft container. As Asian factories return to full production after Chinese New Year, carriers are beginning to add capacity. Only four blank sailings have been announced over the next two weeks, suggesting space will increase and rates could begin firming as volumes recover through March.

On the Transpacific trade, rates moved higher. Shanghai to Los Angeles increased 10% to $2,402, while Shanghai to New York rose 7% to $2,977 per 40ft container. According to Drewry’s Container Capacity Insight, blank sailings have reduced significantly as production in Asia ramps up again, which is expected to support further rate increases in the coming weeks.

Geopolitical tensions are also beginning to influence the market. US and Israeli strikes on Iranian targets have disrupted tanker movements through the Strait of Hormuz, a key route that carries around 20% of global oil supply. Rising crude prices are already increasing bunker fuel costs and war-risk premiums for vessels operating in the region. If the situation escalates, these additional operating costs could begin filtering through into higher container freight rates globally.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”