Welcome to another Logistics News Update.

The story of tariffs is not going away. Just as markets were settling, the United States President Donald Trump introduced a new global tariff of around 10% to 15%. This is a temporary measure, limited to 150 days, and signals continued uncertainty in global trade. See our story of the week for more detail.

Locally, we are seeing ongoing weather-related delays in Cape Town. More concerning is the increase in delays at Port Elizabeth, which has historically been more stable. Durban remains steady, with current delays sitting at around one day, largely due to reduced volumes out of China during the holiday period.

Let’s Learn: What AGOA Means and Why It Matters Now

AGOA gives South African and regional exporters duty free access into the US on thousands of products. It has been a key advantage for industries like automotive, agriculture, and textiles.

But that advantage is now under pressure.

• New US tariffs, even at 10% to 15%, reduce the benefit of duty-free access

• Exporters may still pay more overall despite AGOA

• Countries like Lesotho and Eswatini are highly exposed due to reliance on US markets

• Policy changes can happen quickly, impacting pricing and demand overnight

Playbook:

Do not rely on AGOA alone. Review your US pricing regularly, build flexibility into your contracts, and start developing alternative markets to reduce risk.

Here is your weekly logistics news.

Logistics & Trade Headlines

- Trade policy uncertainty still shaping decisions: Ongoing tariff adjustments and global policy shifts continue to influence sourcing strategies, routing decisions, and long-term supply chain planning.

- Inaugural stone fruit consignment sent to China: South Africa’s first consignment of stone fruit was shipped to China this week. Agriculture Minister John Steenhuisen, accompanied by the People’s Republic of China Ambassador to South Africa, Wu Peng, visited the Freshness First Packhouse in Franschhoek on Wednesday, where the inaugural consignment was prepared for export.

- Transnet reform momentum continues but execution in focus: Following SONA commitments, industry bodies are now pushing for timelines and delivery on private sector participation in ports and rail. The conversation has shifted from policy to implementation.

- Durban performance improving but pressure building again: Pier 2 productivity has held steady, with improved crane moves and reduced vessel waiting times. However, early signs of landside pressure are starting to return as volumes pick up post-Chinese New Year.

- Cape Town congestion risk rising again: Wind disruptions over the past week have led to intermittent stoppages, with exporters already seeing delays on fruit and Agri shipments. Backlogs are expected to build if weather continues.

- Post-Chinese New Year surge starting to show: Carriers are reporting tightening space on Asia to South Africa routes as factories ramp up. Early bookings are increasing, with indications of rate pressure heading into March.

- Peak season surcharges gaining traction: Following CMA CGM’s announcement, other carriers are signalling similar increases on Far East routes. This confirms a likely short-term rate spike linked to capacity constraints.

- Rail constraints remain a structural issue: Bulk exporters continue to report limited rail capacity, forcing more volume onto road. This is increasing costs and adding pressure on port truck flows.

- Global freight rates stabilising with upside risk: After a softer January, indices are showing early signs of firming, particularly on Asia-linked trades. The key driver is controlled capacity and post-holiday demand.

- Airfreight holding steady with balanced demand: Export volumes remain consistent, while imports are slightly softer. Rates have stabilised after peak season, offering short-term predictability for urgent shipments.

- Africa trade corridors gaining real traction: Increased focus on Maputo and regional corridors is translating into real volume shifts, as businesses look for alternatives to traditional South African port routes.

- Trade policy uncertainty still shaping decisions: Ongoing tariff adjustments and global policy shifts continue to influence sourcing strategies, routing decisions, and long-term supply chain planning.

NEWS

Trump tariffs struck down, new US duties follow

21 Feb 2026 – FreightNews

US Tariffs Shift Again Creating New Pressure for SA Trade

Global trade has taken another turn, and this time the impact is immediate for South Africa and the region. The US Supreme Court has struck down parts of the tariff framework imposed under emergency powers, removing some of the steep duties that had been applied to multiple countries. For South African exporters, this initially created a window of opportunity, particularly in cases where tariffs had reached over 30% but that window closed quickly.

Within days, the US introduced a new round of tariffs, reportedly in the range of 10% to 15% on certain imports, applied under a different legal structure, the result is not a return to normal conditions. It is continued uncertainty.

For South African exporters, the reality is clear. While some of the extreme tariffs have fallen away, the cost of accessing the US market remains elevated. Pricing becomes harder to manage, margins are under pressure, and long-term planning becomes more complex.

This does not stop at South Africa. Neighbouring countries such as Lesotho and Eswatini, which rely heavily on preferential trade access, are directly affected. Even without the higher tariffs, the new duties reduce their competitiveness in the US market. Because regional supply chains are interconnected, this has a knock-on effect across the SADC corridor, influencing manufacturing flows, cross-border transport, and volumes moving through South African ports.

From a logistics perspective, this type of policy shift drives behaviour. We typically see exporters accelerating shipments to beat cost increases, followed by periods of slowed demand once higher tariffs take effect. This creates volatility in booking patterns, pressure on space and rates, and a growing need to explore alternative markets such as Europe, the Middle East and intra-Africa trade.

The key issue is not just the tariffs themselves. It is the pace at which policy is changing. For businesses trading into the US, flexibility is no longer optional. Pricing models need to be reviewed regularly, shipment timing becomes critical, and routing decisions carry more weight than before. The US remains a key market, but it is no longer predictable. Source: FreightNews

COMMENT: US trade policy has shifted again, creating short-term opportunity but ongoing uncertainty for global trade.

After the US Supreme Court struck down emergency tariffs, a temporary blanket tariff of around 10% to 15% has been introduced. This is only a short-term measure, with a more structured tariff regime expected to follow. For South African importers and exporters, this does not mean a return to stability. It means a transition period where tariffs may change quickly across different trade lanes.

The impact:

• Tariffs remain in place, but under a different structure

• Short-term pricing opportunities may open on certain routes

• Importers may accelerate shipments to manage risk

• Ongoing uncertainty will continue to affect planning and costs

Bottom line: The environment remains unpredictable. The advantage sits with businesses that plan ahead, secure space early, and stay close to rate and policy changes.

Key Highlights from Last Week’s Discussions – 15th February 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations Summary: – Port Update:

Durban 1 days

Cape Town 14 Days

Port Elizabeth 9 days

Coega 2 Days Source: GoCometys up until the 6th.

1. Port Operations

Port performance softened week on week, driven by Cape Town disruptions and lower Durban volumes.

• Total volumes down around 17%

• Cape Town impacted by wind, power, and system issues

• Durban quieter due to Chinese New Year

• Rail out of Durban up around 24%

Takeaway: Cape Town remains the key risk. Durban is stable but seasonal volumes are down.

2. Air Cargo

Airfreight remains stable at elevated levels.

• Volumes flat week on week

• Inbound up slightly, outbound softer

• Still above last year and pre-pandemic levels

Takeaway: Strong and consistent, with no major volatility.

3. Road and Border Crossings

Conditions improved, but underlying risks remain.

• Queue and processing times improved

• Lebombo volumes slightly up

• Delays still present at key borders like Beitbridge

• Ongoing system and regulatory challenges across SADC

Takeaway: Flow is better short term, but structural issues remain.

4. Ocean Freight and Global Shipping

Market remains under pressure from oversupply.

• Rates down to around $1,959

• Excess capacity continues to weigh on pricing

• Carriers managing supply and consolidating

Takeaway: Weak rate environment continues. Capacity control and consolidation are key drivers.

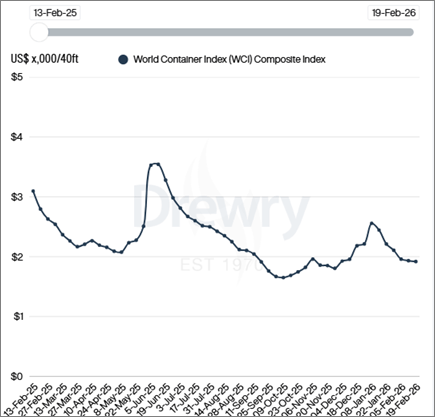

Global Freight Rates

Weekly Container Rate Update – 12 February 2026

Drewry’s World Container Index decreased 1% to $1,919 per 40ft container this week.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”