Welcome to another Logistics News Update.

Logistics & Trade Headlines

- January Container handling figures show rebound consistency: Containerisation gains across South Africa’s sea sector suggest consistently rebounding volumes week-on-week (w-o-w), with consecutive throughput increases of 22.23% and 14.99% supporting January’s port optimism.

- Shipping costs surge could drive higher consumer prices: A major industry survey shows rising shipping and logistics costs are increasingly feeding into consumer goods price inflation, with significant increases already reported in categories like electrical goods and computers. Ongoing supply chain risks contribute to rate volatility rather than temporary spikes.

- Severe winter weather hits global logistics networks: Winter Storm Fern and other cold systems have disrupted freight movement across the United States and Europe, slowing roadway freight, freezing key corridors, and creating port handling delays.

- Logistics funding, tech, and growth stories in industry roundups: Weekly logistics news roundups highlighted growth in drone delivery services, major funding for supply chain tech platforms, and broader transport management trends that are shaping the industry’s direction.

- Global logistics risks and structural challenges persist: Industry commentary from major logistics outlets reports that the market shows surface stability, but underlying fragility remains, especially where capacity, pricing and external risk factors intersect.

- Broader supply chain headlines support ongoing risk planning: Weekly briefs from logistics media have tracked geopolitical, weather and capacity risks, reinforcing that resilience remains a priority for networks and carriers.

- Ocean freight market sees rate correction and volatility: Recent updates show container freight spot rates have eased but volatility remains ahead of Lunar New Year, with shipper behaviour and rate uncertainty shaping booking patterns and capacity plans.

- Infrastructure and inland connectivity challenges continue: Port and inland logistics networks are facing challenges from weather and network congestion, impacting freight flows and creating knock-on delays that could resonate through the first quarter.

- Citrus Growers Advise: BRICS Trade Watch: Countries across the world are actively securing new trade deals to protect their economies yet South Africa’s trade position within BRICS is weakening. Since joining BRICS our trade deficit has widened sharply from R66 billion in 2010 to an estimated R250 billion in 2024 which is a concern. While partners push ahead with better market access progress on key opportunities like a partial trade pact with India has stalled despite clear potential shown in sectors such as citrus. If BRICS is to matter for South Africa it must deliver real trade outcomes that improve competitiveness create jobs and reduce tariffs into key markets.

NEWS

Exporters mull legal remedies over CTCT delays

Source: FreightNews – Staff Reporter

The South African deciduous fruit industry has escalated its concerns over persistent delays at the Cape Town Container Terminal (CTCT), and is now considering legal remedies to recoup losses. According to the industry body Hortgro, ongoing operational underperformance at CTCT is causing “significant and measurable harm” to the export economy, particularly during the peak fruit export season. Since the start of the 2025/26 export season, producers have already recorded direct losses exceeding R350 million, with further exposure building daily as delayed vessels continue to arrive late at destination ports. Export volumes are reported down about 9 percent year-on-year by the second week of the season, while inspection volumes surged by 37 percent, leading to an unusual build-up of nearly 1 700 refrigerated containers in cold storage.

The industry has been forced to divert fruit shipments to alternative ports at substantial cost to maintain market commitments. This includes a 140 percent increase in shipments via Port Elizabeth, additional reefer traffic through Durban, and container rerouting through Walvis Bay. These diversions have incurred extra transport, storage, handling, and quality-related costs that are eroding margins and unsettling rural economies. In formal feedback to Transnet, Hortgro says the terminal’s performance issues are not simply short-term operational shocks or weather-driven problems, but stem from deeper structural failures across labour management, equipment reliability, operational control, and communication. The industry body says incremental fixes are no longer sufficient and is now exploring all remedies to hold parties accountable and protect South Africa’s reputation as a reliable global supplier.

Key Highlights from Last Week’s Discussions – 25TH January 2026

Source: BUSA, SAAFF, and global logistics data

Port Operations Summary: – Port Update:

Durban 2 days

Cape Town 5 Days

Port Elizabeth 13 days*

Coega 3 Days Source: GoComet *Maersk reported 2 days up until the 6th.

1) Port Operations

Headline takeaway: Throughput strengthened further week on week, with weather still the key constraint in Cape Town and improving flow in Durban.

• SA ports handled 60,891 TEUs (↑15% WoW)

• Average throughput: ~8,699 TEUs/day, well above the projected ~7,165 TEUs for the coming week

• Cape Town (CTCT): Windbound early in the week but recovered well, only one vessel at anchorage by weekend

• Equipment availability remained strong in Cape Town with 8 of 9 STS cranes and most RTGs available

• Durban Pier 1: Busier week with higher volumes, some increase in landside time due to throughput uplift

• Durban Gateway Terminal (Pier 2): Strong waterside performance, vessels largely berthing on arrival, but data transparency remains limited

• Rail out of Durban: 4,114 containers (↑28% WoW), recovery after earlier disruptions

Summary: Port performance improved materially with volumes exceeding forecasts. Weather remains the dominant risk in Cape Town, while Durban operations are showing more consistent stability supported by improved rail flows.

2) Air Cargo

Headline takeaway: Airfreight momentum continued, with both inbound and outbound volumes strengthening.

• Total international air cargo: 6,138 tons (↑20% WoW)

• OR Tambo daily averages:

o Inbound: ~564,000 kg/day (↑24%)

o Outbound: ~313,000 kg/day (↑13%)

• International air cargo now 6% above last year levels and 5% above pre-pandemic January averages• Echo Taxilane repairs at ORTIA are underway, but cargo operations are expected to remain unaffected

Summary: Air cargo continues its strong post-holiday recovery, supported by import demand and improving outbound flows. Operational constraints at ORTIA are being managed with limited impact on freight.

3) Road and Border Crossings

Headline takeaway: Border performance improved overall, although pressure remains uneven across corridors.

• Lebombo: ~1,368 trucks/day (↑3% WoW)

o Queue time: ~2.4 hours (↓29%)

o Processing time: ~2.2 hours (↓31%)

• SA median border crossing time: ~7.9 hours (↑15%)

• Broader SADC average: ~4.4 hours (↓8%)

• Estimated weekly indirect cost of border delays: ~R371 million (↑62%), driven by pressure at high-volume crossings

Summary: Border efficiency improved on key corridors such as Lebombo, reducing queue times. However, elevated delays at major crossings continue to drive high systemic costs across the region.

4) Ocean Freight and Global Shipping

Headline takeaway: Freight markets softened further, with overcapacity and weak demand shaping pricing.

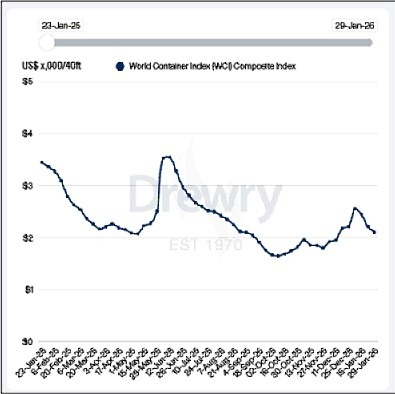

• Drewry World Container Index: $2,212 per 40ft (↓9.5% WoW)

• Global schedule reliability slipped to 62.8%, with average vessel delays just over five days

• Carriers remain cautious on full Suez Canal returns, with continued Cape of Good Hope routing

• Global container demand growth expected to slow further through 2026

• Air cargo rates stabilised around $2.41/kg, with mixed regional performance

Summary: Freight markets are moving into a softer phase, with declining rates and persistent reliability challenges. Carrier routing decisions and geopolitical risk continue to influence capacity and volatility into the year ahead.

Global Freight Rates

Weekly Container Rate Update – 29 January 2026

Drewry’s World Container Index decreased 5% to $2,107 per 40ft container this week.

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”