Welcome to our final Logistics News Update for 2025.

Wishing you and your family a joyous festive season and look we forward to a successful and prosperous 2026.

As this is the final newsletter for the year, we start with a warning for all importers from China.

China has two holidays in February 2026, and this will disrupt the production of goods. Last year, factories started shutting down from around the 22nd of January, which slowed output across most sectors. In preparation, please book your cargo early and plan for delays during this period. This shutdown cycle can disrupt the full supply chain from production to port capacity to vessel schedules.

Trade

- Table grape exports now underway with strong EU pull: The first grape volumes from the Northern Cape have started moving and early demand from the EU is positive. Buyers are taking larger programmes at firmer prices compared to this time last year. Growers are still watching the weather closely as wind delays in Cape Town continue to disrupt stack dates and create rollover risk. Most exporters are building in extra lead time to protect market windows.

- Citrus planning shifts to 2026 with focus on market access: With lemons closing out on a strong finish last week, growers are now looking at 2026 programmes. Attention is on possible tariff changes linked to AGOA’s revision in the US and continuing checks on EU cold treatment compliance. Exporters say any further delays at Cape Town could change early fruit flows for next season.

- US trade risk heightens as AGOA decision approaches: Negotiations around South Africa’s AGOA status remain uncertain. Industry bodies have warned that losing access will hit automotive, citrus, wine and metals first. Exporters are preparing for cost increases until there is clarity. Several producers are reviewing forward contracts and landed pricing models in case tariffs apply from early 2026.

- Grains and oilseeds remain steady across the region: Regional demand for maize and soya is stable. Although Beitbridge had intermittent slow days, traffic moved without major backlogs. Cross-border operators reported reliable flows to Zimbabwe, Botswana and Mozambique. Prices held steady with no major shifts this week.

- Manufacturing exports feel pressure from shipping schedules: Electronics, chemicals and machinery exporters reported some pressure as carriers continue to adjust schedules for Durban and Cape Town. Delays are pushing some exporters to split volumes across services or route via Port Elizabeth when capacity allows. Most expect conditions to improve once the current wind system settles.

- Logistics remains the defining risk factor for all exporters: Weather-related stoppages in Cape Town and equipment shortages in Durban remain the biggest variables across all export sectors. Exporters are planning earlier cut-offs and spreading risk across multiple vessels. The next two weeks will be critical as the wind pattern remains active and volumes pick up ahead of year-end.

What is the news

- Wheat import tariff delay hits wheat farmers: South Africa’s wheat industry is under severe pressure and facing mounting financial strain due to a prolonged delay in reviewing the wheat import tariff, Grain SA has warned.

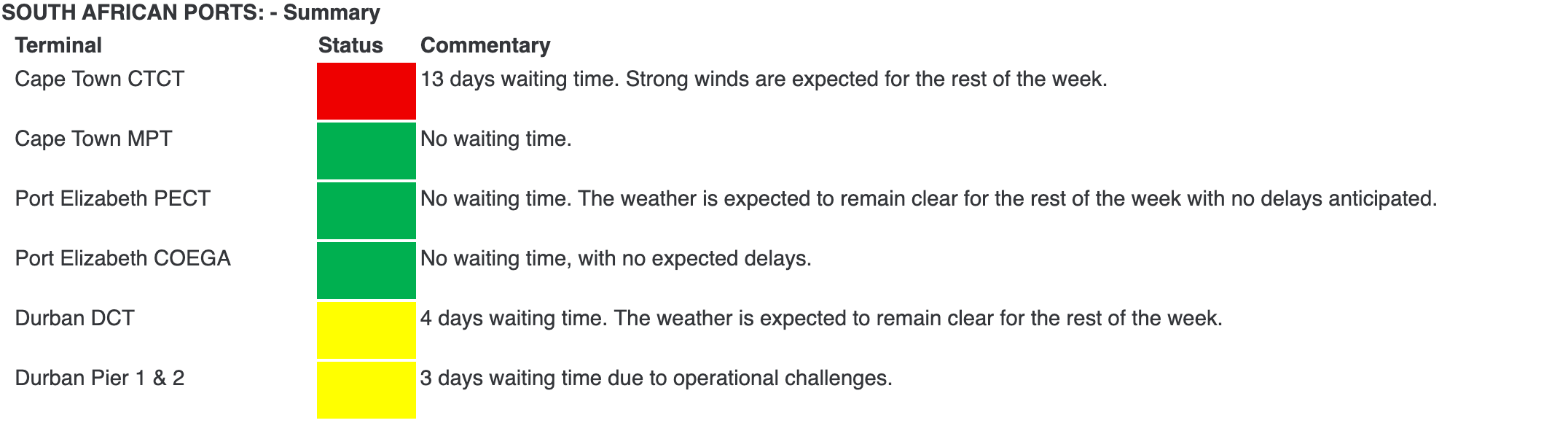

- SA automakers face pressure of rising imports: South Africa’s new vehicle market is surging, but a flood of low-cost imports is squeezing local manufacturers, threatening jobs, and production targets.

- Cape Town still under pressure with another week of wind delays: The south easter remained active and caused repeated stoppages at the Cape Town Container Terminal. Several vessels faced long anchorage waits and slow starts once operations resumed. There were short windows of better productivity, although the overall impact was still heavy. Exporters are planning earlier stack dates because the timing risk remains high.

- Durban holds steady with predictable terminal performance: Durban delivered a more reliable week across Pier 1 and Pier 2. Crane availability improved and there were fewer equipment interruptions, which kept vessel working times stable. Truck flow was consistent, and exporters reported fewer last-minute changes from the lines. This helped improve planning for both imports and exports.

- Port upgrade programmes continue but benefits will roll out gradually: Cape Town’s new RTGs are operating, and more units are due before year’s end. Durban continues with its maintenance cycle to stabilise crane performance and reduce unplanned stoppages. Transnet has indicated that the broader upgrade programme will run into 2026 which means improvements will come in phases rather than all at once.

- Global freight rates show mixed movement as December demand cools: Asia outbound spot rates eased again on some routes, although Europe bound trades remained firm. Carriers are managing capacity aggressively with more blank sailings announced for the next few weeks. This is keeping rates unpredictable and forcing exporters to stay flexible with their routing plans.

- Early season table grapes start moving with solid overseas demand: Growers in the Northern Cape have started cutting and the first exports are moving. EU buyers have shown stronger interest than last year, and pricing is holding. Exporters in the Western Cape will follow once volumes build. The main concern remains the mix of wind delays in Cape Town and tight equipment in Durban which could affect market windows if conditions don’t stabilise soon. Source: FreightNews

Let’s Learn: Why Wind Delays Matter More Than Most People Realise

Weather delays sound simple but they have a much bigger impact on logistics than many exporters expect. Cape Town’s strong south easter is a good example. When the wind reaches unsafe levels, the cranes stop. When the cranes stop, nothing moves. Vessels wait at anchor and every hour lost pushes the shipping schedule out.

Why Wind Delays Disrupt Your Plan

When a vessel falls behind schedule, the terminal must reshuffle stacks and adjust cut off times. Exporters often lose their planned stack window, which means the cargo either rolls or must be rushed into the terminal at the last minute. This increases transport cost and raises the risk of missing the market window.

How One Delay Affects the Whole Chain

A single day of wind can trigger several knock-on effects.

• Vessels bunch up at anchor

• Stacks shift and exporters must rebook

• Carriers push back ETDs to recover time

• Downstream ports adjust berthing plans

This is why wind delays sometimes look small on paper but create real pressure across the whole supply chain.

Why Some Ports Cope Better

Durban and Ngqura are less exposed to strong seasonal winds. Even with equipment challenges, they often deliver a more stable working rhythm. Cape Town depends heavily on weather windows so operations can swing from productive to closed within minutes.

What Exporters Should Do

• Build early stack dates into your plan, especially for fresh produce

• Spread bookings across two services when possible

• Keep your buyer informed so they can manage expectations

• Watch weather forecasts and carrier advisories closely

Small planning steps protect your market window when conditions change suddenly.

Key Point

Wind delays are not only about the hours lost. They change the whole timing of the supply chain. When you understand how these delays cascade through the system, you can plan better and avoid costly surprises.

NEWS

SA port cargo volumes up

5 December 2025 – By Lyse Comins

South African ports recorded a solid increase in cargo volumes this past week with container throughput rising by about nine percent. Daily averages improved and the terminals handled stronger flows across most regions. This indicates healthier demand as we approach year-end and demonstrates that the network can improve performance when conditions remain stable.

Cape Town continued to face pressure from strong winds which limited productivity. The south easter forced several stoppages and more than forty operational hours were lost. Although there were short periods of improvement, the overall impact was slower vessel working times and longer anchorage delays. Exporters are still planning with caution because the wind pattern remains active.

Durban delivered a more stable operational week. Crane deployment improved and there were fewer equipment problems across Pier 1 and Pier 2, which supported better vessel working times. Truck movement was more predictable, and exporters experienced fewer short notice changes to stack dates. Durban remains the most reliable performer in the current cycle.

Rail uplift did not match the rise in port volumes. The Durban rail movement dropped as line availability issues continued, which pushed more cargo onto the road network. The added pressure on trucking schedules and inland depots is likely to continue until the rail system stabilises. Planning still needs to take these constraints into account.

Overall conditions show a mix of positives and ongoing challenges. Higher port volumes are encouraging, although weather delays in Cape Town, equipment constraints in Durban and weak rail performance keep the environment unpredictable. Importers and exporters should allow extra time around cut-offs and consider spreading bookings to reduce the risk of rollovers.

Source: Adapted from FreightNews

Key Highlights from Last Week’s Discussions – 16th November 2025

Source: BUSA, SAAFF, and global logistics data

1. Port Operations

South African ports handled 75,462 TEUs, an increase of 9 percent from the previous week’s 69,058 TEUs.

The daily average improved to 10,780 TEUs.

Breakdown

• Durban Pier 2: 35 156 TEUs (↓4 percent)

• Durban Pier 1: 8 935 TEUs (↓27 percent)

• Cape Town: 9 708 TEUs (↑570 percent) as the weather began to ease

• Ngqura: 12 303 TEUs (↓6 percent)

• Port Elizabeth: 2 563 TEUs

• Other terminals: 6,797 TEUs (↑22 percent)

Main Issues

• Cape Town lost 40 operational hours due to wind

• Durban faced equipment shortages that restricted crane and straddle availability

• Eastern Cape ports were slowed by vacant berths and equipment issues

• Richards Bay saw adverse weather with reduced coal throughput

Summary

A more stable week across the network as the weather eased in most regions. Cape Town recovered strongly. Durban remained constrained by equipment. National throughput improved but still sits below projected capacity.

2. Air Cargo

International air freight remained firm, with November closing as a record month for OR Tambo.

• Inbound: 4 845 371 kg (↓3 percent)

• Outbound: 2 937 406 kg (↑2 percent)

• Total: 7 782 777 kg (↓1 percent)

November Performance

• Air cargo up 20 percent month on month

• Air cargo up 21 percent year on year

• November is now the highest month recorded since tracking began

• Operations affected by hail and water damage to several facilities at OR Tambo

Volumes remain well above 2024 and pre-COVID levels.

3. Road and Border Crossings

Conditions tightened modestly across the region.

Lebombo Border

• Truck traffic: 1,349 trucks per day (↓2 percent)

• Queue time: 6.4 hours

• Processing time: 6.2 hours

Regional Border Trends

• Median SA border crossing time: 12.7 hours (↑6 percent)

• SADC region crossing time: 5.7 hours (unchanged)

• Four borders averaged close to a full day to cross

Estimated Indirect Cost of Delays

• Approx $36.4 million (R630 million) for the week

• Up from $35 million the previous week

Hotspots remain Zimbabwe, Zambia and N3 closures linked to incidents and blockades.

4. Ocean Freight and Global Shipping

Global Port Throughput

Drewry’s Global Container Port Throughput Index:

• Down 1.4 percent month on month

• Up 4.0 percent year on year

Regional Index Movements

• Greater China: down 3.1 percent m/m, up 3.5 percent y/y

• North America: down 3.9 percent m/m, down 1.0 percent y/y

• Europe: up 2.1 percent m/m, up 6.0 percent y/y

Rates and Market Structure

• World Container Index: down 2.5 percent to $1 806 per FEU

• Charter market stable at 2,184 points

• Oversupply risk building as global TEU-mile demand slows

• CMA CGM planning a limited return to the Suez routing

5. International Air Cargo Industry

• Global spot rates up 2 percent week on week to $2.93/kg

• Asia Pacific to Europe lanes saw further increases

• High season demand linked to Black Friday and Cyber Monday lifted global rates

Summary

South Africa saw a more stable operational week with strong port throughput and continued momentum in air freight. November air cargo statistics show clear demand strength. Border performance weakened slightly which increased indirect costs. Globally, throughput softened month on month but stays stronger year on year with Europe showing the most improvement.

Port Operations Summary: – Port Update:

Global Freight Rates

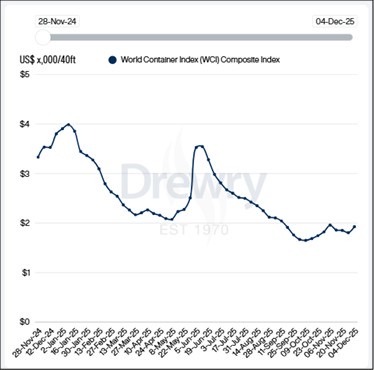

Weekly Container Rate Update – 4 December 2025

The Drewry World Container Index increased by 7 percent this week to 1,927 dollars for a 40-foot container. This is a noticeable shift after several weeks of softer pricing and reflects firmer demand and carrier attempts to lift market levels.

On the Transpacific head haul, spot rates moved higher. Shanghai to Los Angeles increased to 2,256 dollars and Shanghai to New York rose to 2,895 dollars. These increases follow a period of declining rates and come as carriers adjust capacity and apply more frequent general rate increases. Asia to Europe pricing also strengthened this week. Shanghai to Genoa climbed to 2,648 dollars and Shanghai to Rotterdam rose to 2,241 dollars. Carriers continue to push for higher FAK levels to improve yield ahead of the annual contracting season.

Although rates increased across most major lanes, the market remains volatile. Any return of more vessels to the Suez route could add capacity to the system, which may trigger further pricing swings. For now, the short-term trend is firmer but still sensitive to changes in demand and vessel deployment. Source: Drewrey

Disclaimer: The information provided in this newsletter is based on reliable sources and has been carefully verified. This Logistics News is distributed free of charge. If you wish to unsubscribe from our mailing list, please reply to this email with “unsubscribe” in the subject line. Please note that all content is adapted or directly quoted from its original sources. We take no responsibility for any inaccurate reporting; we are only adapting the news for you.

This week’s news was brought to you by:

FNB First Trade 360 – a digital logistics platform and Exporters Western Cape

“This information contained herein is being made available for indicative purposes only and does not purport to be comprehensive as the information may have been obtained from publicly available sources that have not been verified by FirstRand Bank Limited (“FRB”) or any other person. No representation or warranty, express, implied or by omission, is or will be given by FRB, its affiliates or their respective directors, officers, employees, agents, advisers, representatives or any other person as to the adequacy, reasonableness, accuracy or completeness of this information. No responsibility or liability is accepted for the accuracy or sufficiency thereof, or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. In particular, but without limitation, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, targets, estimates or forecasts and nothing contained herein should be, relied on as a promise or representation as to the past or future. FRB does not undertake any obligation to provide any additional information or to update the information contained herein or to correct any inaccuracies that may become apparent. The receipt of this information by any person is not to be taken as constituting the giving of any advice by FRB to any such person, nor to constitute such person a client of FRB.”